Research papers

|

M&A Trends & Intelligence

Jelle Stuij

Thank you for taking the time to read the first edition of the Dealmaker Insights Report for the Nordics. This report is the result of comprehensive research conducted by Dealsuite, the leading platform for M&A transactions. It features detailed data concerning the Nordic mid-market (companies with revenues between €1 million and €200 million) and includes valuable insights from Nordic dealmakers. 121 Nordic M&A advisory firms contributed their expertise to this research.

The assessment period is the second half of 2024 and an outlook towards 2025.

The aim of this study is to create periodic insights that improve the Nordic market’s transparency and to serve as a benchmark for M&A professionals. We are convinced that sharing information within our network leads to an improved quality and volume of deals.

After a period marked by high interest rates and inflation, 2024 saw the start of an uneven recovery across Europe, although the pace of recovery varied by region. In the first half of the year, most European countries experienced an increase in M&A activity. On average, this activity level remained stable through the second half of the year. M&A advisors in the Nordics reflected on the number of transactions closed in H2-2024 and reported on the level of activity. The results are presented in Figure 1.

In the second half of 2024, M&A activity in the Nordics continued at a pace similar to the first half. A substantial majority of advisors (71%) reported the activity level as moderate.

Figure 2 offers a view of the diverse landscape of buyer types in M&A transactions. It categorizes the participants into Strategic/Corporate buyers, Financial investors, and Other buyers, which includes scenarios such as Management Buy-Ins (MBI) and Management Buy-Outs (MBO). The percentages shown depict how frequently each type of buyer is involved in deals, providing insight into current trends and shifts in the M&A market.

Strategic/Corporate buyers and Financial investors are almost equally active in the Nordic M&A mid-market, each participating in a significant portion of the transactions. 11% of buyers are involved in Management Buy-Ins (MBIs), Management Buy-Outs (MBOs), and search funds. Notably, there has been a surge in search funds, driven not only by increasing recognition of their potential and benefits, such as improved expertise, but also by enhanced access to deal flow and crucial funding (Dealsuite Trends Report, 2024).

Figure 3 presents average European EBITDA multiples by sector. Dealsuite has conducted research on valuation multiples for mid-market transactions across European countries for over a decade. In Q1 2025, transaction data collection commenced for Norway, Sweden, Finland and Denmark. A dedicated report on M&A mid-market multiples in the Nordics is scheduled for publication by the end of 2025. Please note that data from the Nordics is not yet included in the figures presented below.European sell-side advisors defined the average EBITDA multiple by industry. Multiples vary between 3.5 (Retail Trade) and 7.7 (Software Development). This means that theaverage price of an SME can vary significantly, depending on the industry.

The size of a company plays a crucial role in determining multiples in business valuation across Europe. For small and medium-sized enterprises (SMEs), accurately quantifying the impact of the Small Firm Premium is essential. This is particularly relevant for businesses with an EBITDA ranging from €200,000 to €10,000,000.

Studies have shown that smaller companies face a higher likelihood of not achieving their expected cash flows (Damodaran, 2011; Grabowski & Pratt, 2013). This can be attributed to factors such as reliance on specific customers or suppliers, or dependence on unique technical expertise that may be lost if key employees leave. Such vulnerabilities can significantly impact a company’s returns and, consequently, its valuation. The elevated risk premium associated with smaller businesses, known as the Small Firm Premium, leads to a reduction in value. As a result, EBITDA multiples for larger companies tend to be higher on average compared to those for smaller companies.

The results of the Dealsuite survey confirm once again that companies with a low EBITDA have a lower multiple than those with a high EBITDA. The influence of company size on EBITDA multiples is further illustrated in Figures 4a and 4b.

On average, the difference in EBITDA multiples between companies with a normalized EBITDA of €200,000 and €10,000,000 is 3.3 (3.9 compared to 7.2).

Cross-border M&A offers multiple benefits, such as more favorable selling conditions for sellers, lower purchase prices for buyers, market expansion, and enhanced global competitiveness. To better understand the dynamics in the Nordics, advisors were surveyed regarding the geographical distribution of their deal partners. The survey results, presented in Figure 5, show whether these deal partners are predominantly national or international, providing insight into the current trends and preferences in the Nordic M&A landscape.

4 out of 10 deals involve a foreign deal partner (42%). This percentage indicates the level of international engagement in the Nordic M&A market. Additionally, the majority of sellers in the Nordics are open to an international buyer. According to the advisors, 57% of their clients are welcoming to a foreign buyer. This broadens their opportunities to find the most suitable buyer as well as a possible higher selling price.

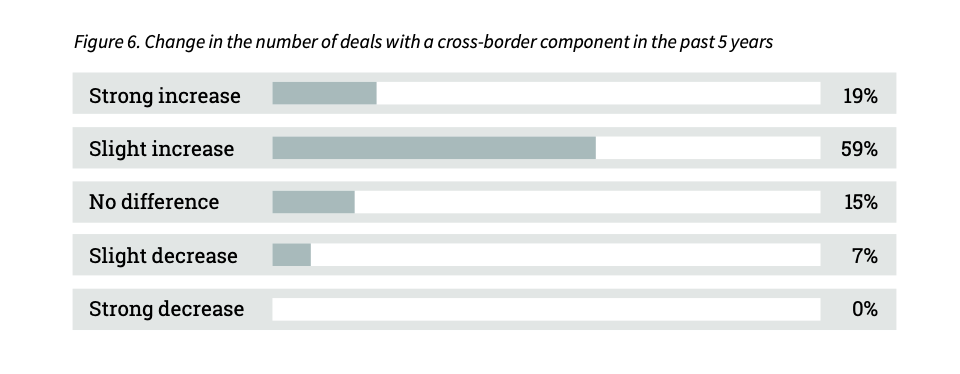

The M&A market is becoming increasingly transparent with borders fading and digitalization making it easier to connect across countries. The vast majority of advisors (78%) have witnessed an increase in the number of transactions with a cross-border component in the Nordics SME sector in the past 5 years.

These results align with findings from the European Private Equity Monitor 2025, where European Private Equity professionals are increasingly acknowledging the benefits of cross-border M&A. On average, in 87% of instances, a PE firm is open to selling to a foreign buyer. A significant motivation for involving foreign parties in the acquisition or sale of a company is the potential to secure a more favorable price, due to valuation differences between countries. This can mean achieving a higher sale price or obtaining a lower purchase price.

According to Nordic advisors, foreign dealmakers should consider acquiring or selling to Nordic companies for several compelling reasons. The Nordic region is characterized by its strong, stable economies and a low-risk business environment, making it an attractive landscape for international transactions. Companies in the Nordics are often praised for their high quality, robustness, and innovative capabilities, particularly in areas like digitalization, AI, medical equipment, and sustainability.

The region boasts a well-educated workforce, high productivity levels, and a transparent regulatory system that enhances operational stability. Additionally, the Nordic countries have a significant degree of internationalization, with many companies actively involved in both exports and imports. This not only positions them well for leveraging their local market advantages but also for utilizing their competencies on a global scale.

Infrastructure in the Nordics is well-developed, and the political climate is stable, offering growth opportunities and a safe transaction environment. The competitive currency rates enhance the financial appeal for transactions in USD or EUR.

Overall, the combination of economic stability, advanced capabilities, and favorable market conditions makes the Nordic region a prime candidate for foreign investors looking to expand their reach or strengthen their international presence.

Certain sectors are emerging as hotspots for mergers and acquisitions (M&A), drawing significant interest due to their robust growth and transformative potential, while others may experience a decline. Figure 7 highlights the sectors expected to boom, capturing the attention of investors looking for opportunities. Conversely, Figure 8 ranks the sectors anticipated to see a downturn in M&A activity, reflecting shifting economic factors and market priorities. Understanding both the surges and declines in M&A activity provides a strategic advantage and offers valuable insights into future industry trends and overall market dynamics.

The IT services sector is projected to lead in transaction growth in 2025, with several key drivers fueling this trend. According to respondents, the sector offers significant opportunities due to ongoing automation, digitalization, and the integration of artificial intelligence. The sector continues to be a central focus for many private equity firms and venture capitalists. As companies across all industries increasingly digitize, this sector represents a growth market with both short-term and long-term potential.

In contrast to the booming IT services sector, several industries are anticipated to see a decline in M&A activity in 2025. Leading this trend is the Retail Trade sector, which faces significant challenges according to respondents, such as increased vertical integration, advancements in digitalization and AI, and the rapid growth of e-commerce. These factors, alongside reduced consumer spending power, are shapingthe landscape. Furthermore, these issues, coupled with investor concerns over consumer sentiment and the viability of physical retail spaces, are expected to notably reduce transaction volumes.

The Construction & Engineering, Automotive, Transportation & Logistics, and Hospitality and Tourism sectors are also expected to experience a slowdown in M&A activities.

In 2025, the M&A landscape in the Nordic region is expected to be shaped by several significant trends. Firstly, the integration of AI and increased automation are set to transform business operations, driving acquisitions in technology and software, particularly in sectors like SaaS and ICT. Additionally, there is an anticipated surge in private equity exits (Dealsuite Private Equity Monitor, 2025).

Despite ongoing geopolitical uncertainty, financial markets are still anticipating lower interest rates. This economic environment will likely lead to an increased focus on fundamental company performance and could narrow international expansion primarily to markets within the EU where business models are more aligned.

Defense-related industries and sectors linked to disruptive technologies are also expected to see a heightened focus due to their strategic importance. Overall, the M&A activity in the Nordics is expected to increase, supported by a growing economy and favorable financial conditions.

Assessing the performance of the Nordic M&A mid-market is based on many factors, including the willingness of entrepreneurs to sell their businesses, funding availability, and macroeconomic developments. An interpretation of these factors is needed to determine how the market will develop. The survey included both assessments of the M&A mid-market in H2-2024 (retrospective) and H1-2025 (projection).

The opinions on the performance of the overall Nordic M&A mid-market in H2-2024 are evenly split between positive and negative impressions, though they lean more towards the positive. Half of the advisors viewed H2-2024 with a slightly negative to negative impression, while the other half held a slightly positive to very positive view of the market during the same period.

The M&A mid-market in the Nordics looks set for a robust 2025, fueled by several positive economic and market trends. With interest rates expected to decline, alongside controlled inflation, the financial landscape is becoming more favorable to transactions. Companies in the region are performing well, adding to the attractiveness of the market.

According to respondents, these factors, combined with the availability of dry powder from investors and a general alignment in price expectations between buyers and sellers, signal a year where strategic and financial buyers are ready to act. The result is an anticipated uptick in M&A activities, driven by the need to deploy capital and seize growth opportunities, particularly in flourishing sectors like AI and digital transformation.

77% of advisors express optimistic expectations for the first half of the year.

The majority of M&A transactions occur within the mid-market segment. For the purposes of this M&A report,mid-market companies are defined as those with revenues between €1 million and €200 million. The underlying survey for this report was distributed to 302 M&A advisory firms, considering their combined input, they represent an essential part of the M&A mid-market. Out of the total of 302 advisory firms, we received responses from 121 M&A advisory firms.

Sources used:

• 121 survey responses from M&A advisory firms in the Nordic region

• Dealsuite M&A Monitors 2015 - 2025

• Dealsuite transaction data 2015-2025

• Dealsuite Trends report 2024

• Field, A. (2011) Discovering Statistics SPSS. Third edition, SAGE publications, London. 1 -822

• Damodaran (2011). Equity Risk Premiums (ERP).

• Graham, J., Harvey, C., Puri, M., 2010. Managerial Attitudes and Corporate Actions. Working Paper, Duke.

• In-depth contributions from 604 leading European M&A advisory firms

This research was conducted by Jelle Stuij and Roos Bijvoet. For further questions, please contact Jelle Stuij.

To discover how Dealsuite can benefit your business - contact Lars Brouwer, Teamlead Nordics.

.png)

Grow your network. Find more deals.

Science Park 106

1098 XG Amsterdam

Netherlands

© 2026 Dealsuite. All rights reserved.

.png)