|

Jelle Stuij

This report marks the third edition of the annual European Private Equity Monitor, a research initiative by Dealsuite, Europe’s leading platform for M&A transactions. It offers key insights into the latest statistics and trends shaping the European Private Equity landscape. This study draws on the expertise of 532 Private Equity professionals from leading firms throughout Europe.

The aim is to offer entrepreneurs and industry specialists valuable insights that support a well-informed understanding of the Private Equity landscape. Dealsuite has produced regional and international M&A reports for many years, driven by our belief that sharing knowledge within our network enhances both the quality and the volume of M&A transactions.

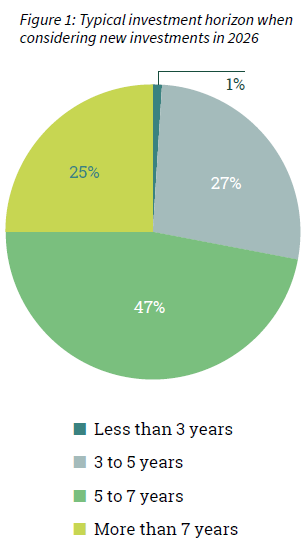

The length of an investment period varies between firms and is shaped by a mix of company-specific elements and broader economic influences. Factors such as progress toward growth objectives, overall market conditions, buyer interest, and opportunities for value creation all affect when an exit may occur (Warren, Geoffrey J., 2014). In this edition of the Private Equity Monitor, Dealsuite asked PE professionals about their expected investment horizon for new deals in 2026. The results are presented in Figure 1.

Only 1% of PE professionals consider an investment horizon of less than 3 years. The majority of PE professionals consider a holding period of more than 5 years (72%).

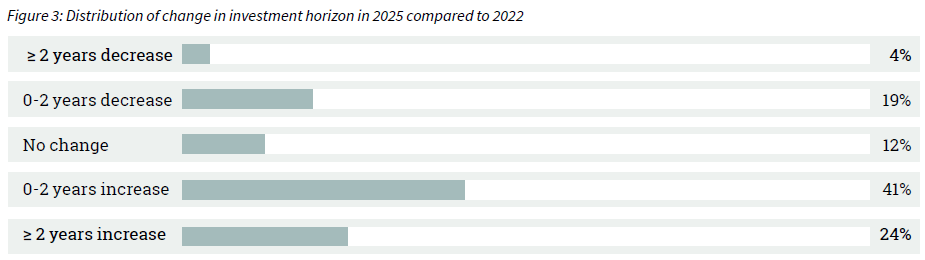

The planned exit of a portfolio company can be influenced by numerous factors, which may cause shifts or delays. In recent years, the inflation, rising interest rates, and geopolitical tensions have all meaningfully affected market conditions and, with that, the ability to exit. Figure 2 illustrates how investment horizons have evolved between 2022 and 2025.

62% of PE professionals indicate that their investment horizon has lengthened over the past three years. Meanwhile, 15% observed a shorter horizon between 2022 and 2025, and 23% reported no change. Overall, the average investment horizon rose by 5 months.

Figure 3 shows the distribution of responses on change in investment horizon. 41% of respondents report an increase in investment horizon between 0 and 2 years. 24% of respondents report an increase in investment horizon of 2 or more years. 4% of respondents notice a decrease in investment horizon of 2 or more years.

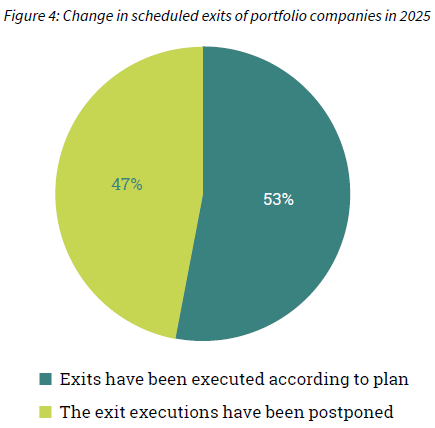

Exit timing is a critical component of the Private Equity value creation cycle, closely linked to returns and portfolio strategy. Figure 4 shows the change in scheduled exits of portfolio companies in 2025. Among respondents who had planned an exit for 2025, 53% have executed their exits as intended, while 47% report postponing the planned transactions. With 48% of exits postponed last year as well, it is clear that exit delays remain a recurring pattern in the current market environment.

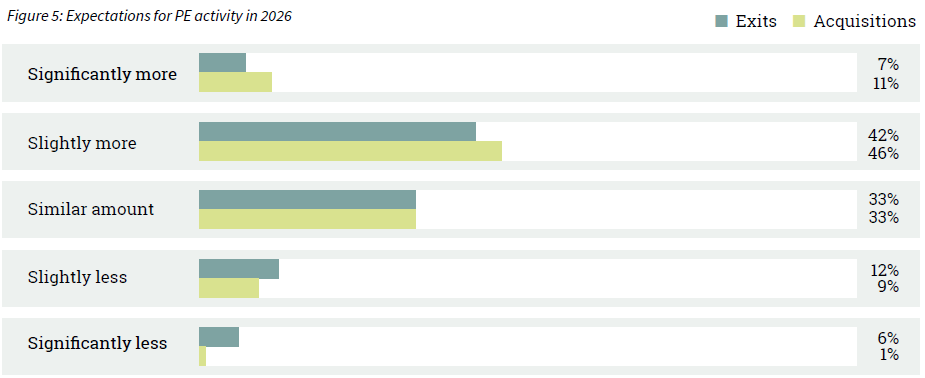

Expectations for 2026 indicate a generally positive outlook for deal activity. Looking ahead to 2026, 49% of PE professionals expect exit volumes to rise, with 33% predicting activity will remain in line with 2025. For acquisitions, sentiment is even more optimistic: 57% of respondents expect higher activity in 2026.

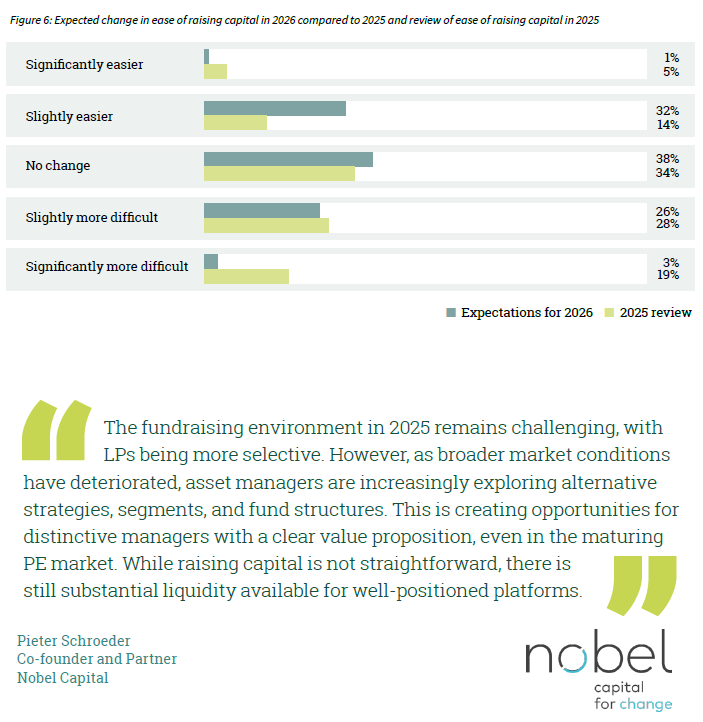

Factors such as inflation and high interest rates heavily impact the ability to raise capital. In 2025, 47% of PE professionals reported that raising capital had become slightly or even significantly more challenging compared to the previous year. The expectations for 2026 are mixed, 29% of respondents expect raising capital to become more difficult, while 33% expect it will become easier.

Last year, PE professionals indicated openness to selling to a foreign buyer in 87% of exits, and in

37% of cases would actually complete an international sale. As the M&A landscape becomes more transparent, with borders increasingly fading and digitalisation making cross-country connections easier, cross-border activity is steadily gaining ground.

A key reason to involve foreign parties in the acquisition or sale of a company is the potential for more favourable pricing, whether achieving a higher selling price or securing a lower acquisition price.

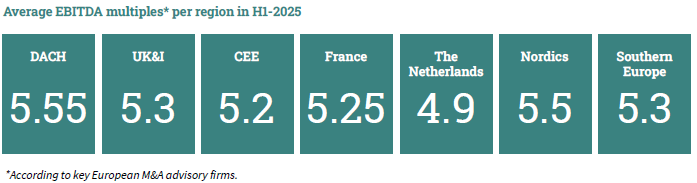

Data from the biannual M&A Monitor of September 2025, shows that average EBITDA multiples differ substantially across European markets. As a result, involving a foreign buyer or seller can often lead to a better deal.

In 2023, only 3% of European PE professionals reported using AI on a regular basis. By 2025, this share has risen sharply, with 41% now describing AI as common practice. At the same time, non-usage has declined significantly: whereas 53% had not used AI at all in 2023, this figure has dropped to 11% in 2025.

This shift shows that in just two years, AI has evolved from a niche tool to a widely embedded part of European mid-market M&A practices.

In September 2025, Dealsuite conducted research on the use of AI among M&A advisors active on the buy- and sell-side in mid-market transactions. According to the European M&A Monitor, 19% of M&A advisors have not yet used AI, compared with only 11% of PE professionals. While AI adoption has increased significantly across both groups in recent years, PE professionals appear to be integrating AI into their processes at a slightly faster pace.

AI tools are increasingly being introduced across critical stages of the PE workflow, with some processes already seeing higher adoption and clearer benefits than others.

In 2025, AI is viewed as most valuable in market research, with 78% of European PE professionals reporting significant added value and only 3% seeing no benefit. Faster target evaluation, and legal document creation or evaluation also rank highly. Post-merger integration is considered to benefit to a lesser extent.

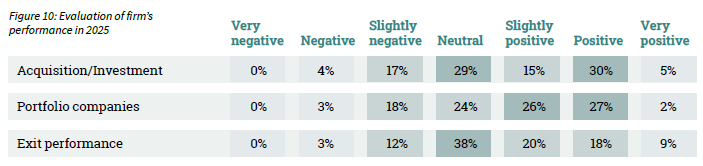

Assessing the performance of the Private Equity market relies on a combination of factors, such as the ease of raising capital, the availability of businesses willing to sell, the exit potential of portfolio companies, macroeconomic conditions, and overall portfolio performance. An interpretation of these factors is needed to determine how the market will develop. This research captures both a retrospective assessment of the 2025 PE market and expectations for 2026. Figure 10 presents the performance of PE activities in 2025.

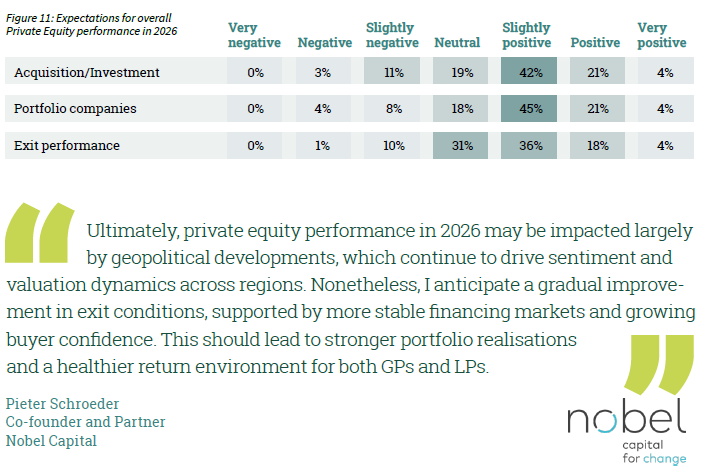

Figure 11 shows the expectations for overall Private Equity performance in 2026. Sentiment toward portfolio companies performance is clearly optimistic, with 70% of respondents anticipating positive results. In total, 58% of respondents anticipate positive exit performance in 2026.

The aim of this study is to provide valuable insights about Private Equity to entrepreneurs and other professionals in the sector, contributing to a positive reflection of the Private Equity domain. The survey that was the basis for this Private Equity monitor was sent to 4,000 PE professionals operating in Europe. Considering their combined input, they represent an essential part of the Private Equity market in Europe. Out of the total of 4,000 PE professionals, we received in total 532 responses.

Sources used:

• Dealsuite transaction data 2015-2025

• Dealsuite M&A mid-market trends report 2025

• Dealsuite M&A Monitors 2015 - 2025

• Dealsuite European Deal Terms Report 2025

This research was conducted by Jelle Stuij and Roos Bijvoet.

For further questions, please contact Maarten Reinders, CCO Dealsuite.

.png)

Grow your network. Find more deals.

Science Park 106

1098 XG Amsterdam

Netherlands

© 2026 Dealsuite. All rights reserved.

.png)

.png)