Forschungsarbeit

|

Jelle Stuij

Thank you for taking the time to read this seventh edition of the European M&A Monitor. This report consolidates research conducted by Dealsuite, the leading European platform for M&A transactions. It provides statistics and trends for the European M&A mid-market (enterprises with a revenue between €1 million and €200 million) over the second half of 2025.

For this research, 848 leading mid-market M&A advisory firms across Europe shared firsthand insights exclusively with Dealsuite, based on the transactions they completed in H2-2025. Their contributions, combined with proprietary Dealsuite data and reports, form the foundation of this study. Since many of these deals are not publicly disclosed, Dealsuite’s network provides unparalleled visibility into the otherwise opaque European mid-market.

The aim of this study is to create periodic insights that enhance the transparency of the European market and serve as a benchmark for M&A professionals. While we have been publishing local/regional reports for several years, this is the seventh time we publish this pan-European report, with a focus on inter- regional differences as well as similarities. We are convinced that sharing information within our network leads to an improved quality and volume of deals.

European M&A activity increases

After years of volatility, uncertainty is the new normal in the M&A market. Dealmakers, particularly in the SME segment, are proving resilient and well-adapted to this structural change. To safeguard transaction progress in an unpredictable market environment, dealmakers are increasingly applying flexible deal structures. According to the Dealsuite M&A Deal Terms Report, there is a clear increase in the use of deferred payments and other forms of risk-sharing.

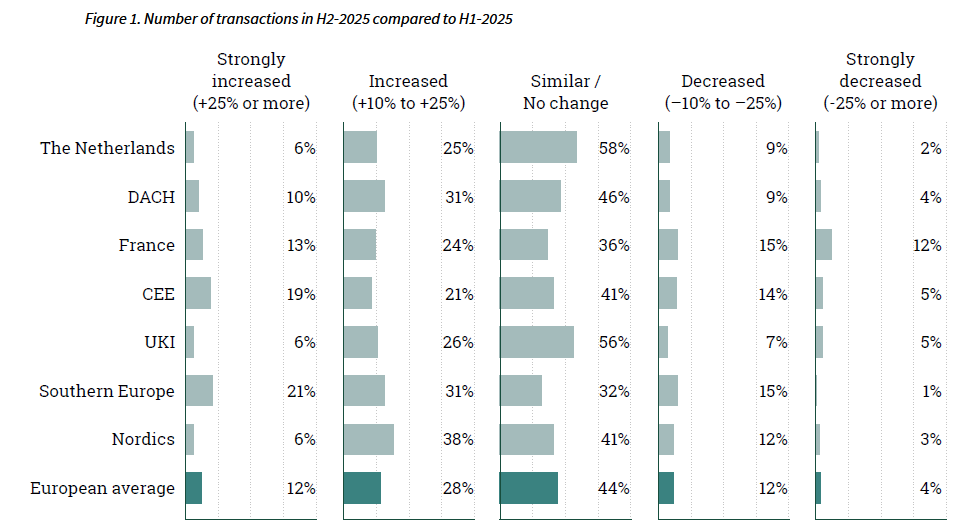

In the second half of 2025, moderate increases in transaction activity outweighed reported declines across all monitored European regions. In Southern Europe, more than half of participating advisors reported an increase in the number of transactions. In the Netherlands, one in three advisors reported higher deal activity.

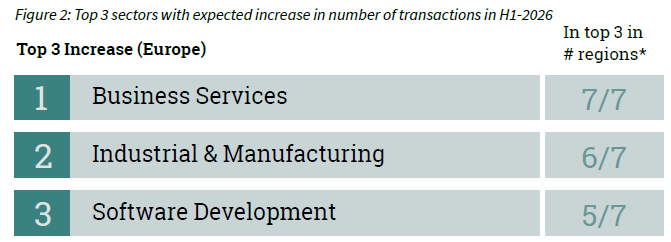

The Business Services sector is expected to drive transaction growth

To assess expected market developments, M&A advisors were asked which sectors they anticipate to have the largest increases or decreases in deal activity during the first half of 2026. Each respondent selected one sector. The results are presented in two tables, highlighting the three sectors most frequently cited for expected increases and decreases in transaction volumes.

When asked which sector is expected to see the largest increase in transaction volume, M&A advisors largely reaffirmed their H1-2025 views. The Business Services, Industrial & Manufacturing and Software Development sectors are expected to drive transaction growth.

Expectations regarding declining transaction activity remain concentrated in a limited number of sectors. Similarly to H1-2025, M&A advisors identified Retail Trade as the sector likely to see the largest decrease in deal volume in H1-2026, followed by Construction & Engineering and Hospitality & Tourism.

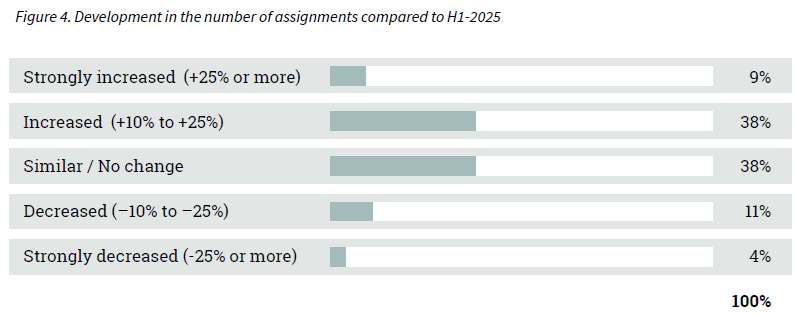

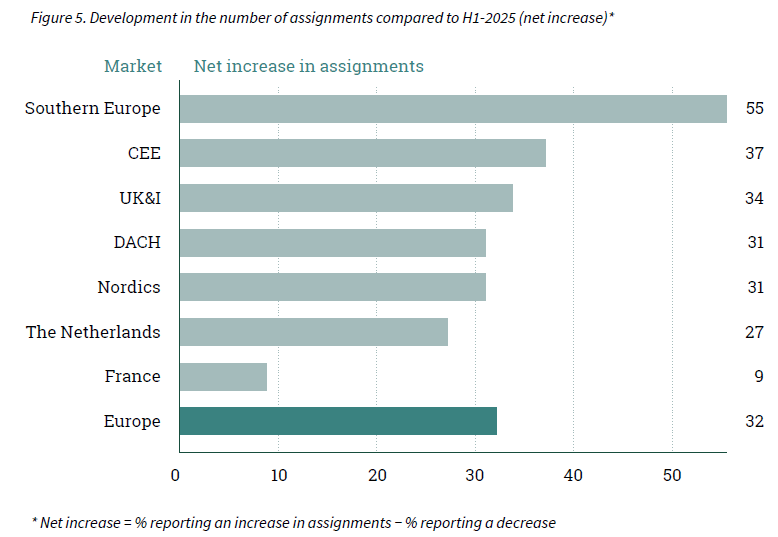

Substantial increase expected in the number of M&A transactions

An increase or decrease in assignments received by advisory firms provides insight into expected deal flow and market sentiment. After an upward trend in the number of assignments in the first half of the year, advisors stated the same trend for H2-2025. The results are shown in Figure 4 below.

These are assignments received in the second half of 2025 and converted into transactions during the same period. In some cases, these assignments will only lead to a deal somewhere in 2026, or could still be terminated.

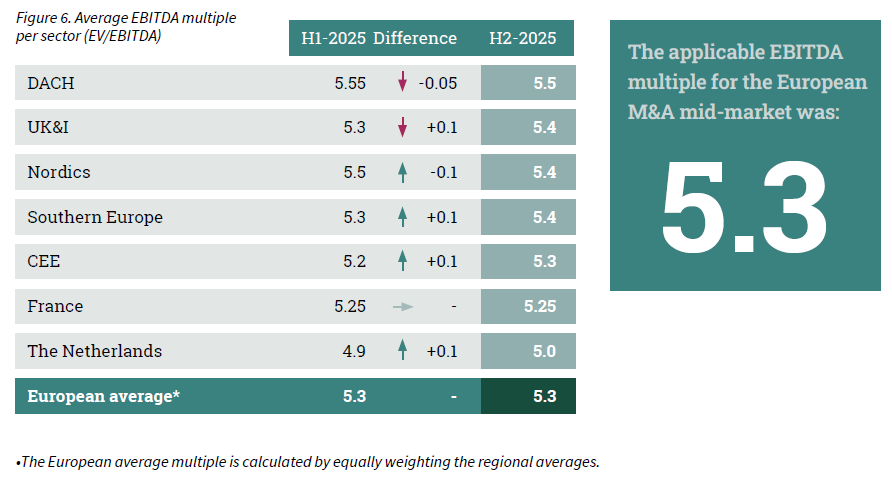

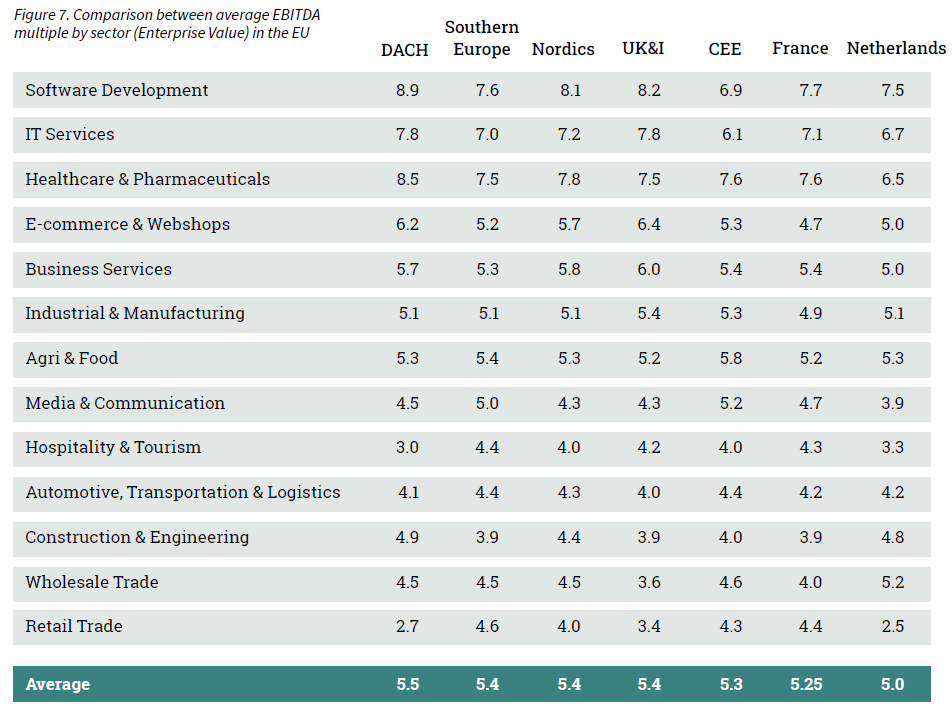

The average European EBITDA multiple remained stable at 5.3

EBITDA multiples serve as a widely accepted benchmark for business valuation, offering insight into what buyers are prepared to pay across different sectors. Since early 2015, Dealsuite has published semi- annual updates on average sector multiples, reflecting the typical EBITDA multiple paid for companies within each industry.

For this study, respondents provided their current observations of transaction multiples, informed by their adjusted market insights. These findings, shown in Figure 6, represent multiples based on the enterprise value (EV) of the acquired companies.

A business valuation is inherently company-specific and depends on a wide range of factors, including growth prospects, profitability, market position, and risk profile. A multiple, on its own, does not constitute a complete valuation methodology, but it serves as a useful cross-check, particularly when assessing comparable transactions in the near term.

The average European EBITDA multiple remained stable at 5.3 in H2-2025. Regional differences do exist. The average Nordic multiple slightly decreased from 5.5 to 5.4, while the multiples for Southern Europe, the Netherlands, CEE and the UK&I saw an increase. The French multiple remained stable and the DACH multiple noted a small drop.

A comparison of EBITDA multiples between different countries highlights the advantages of cross-border deals. For example, it can be beneficial to buy a particular company abroad or to sell a company to an international buyer. Figure 7 shows the differences in EBITDA multiples between European regions.

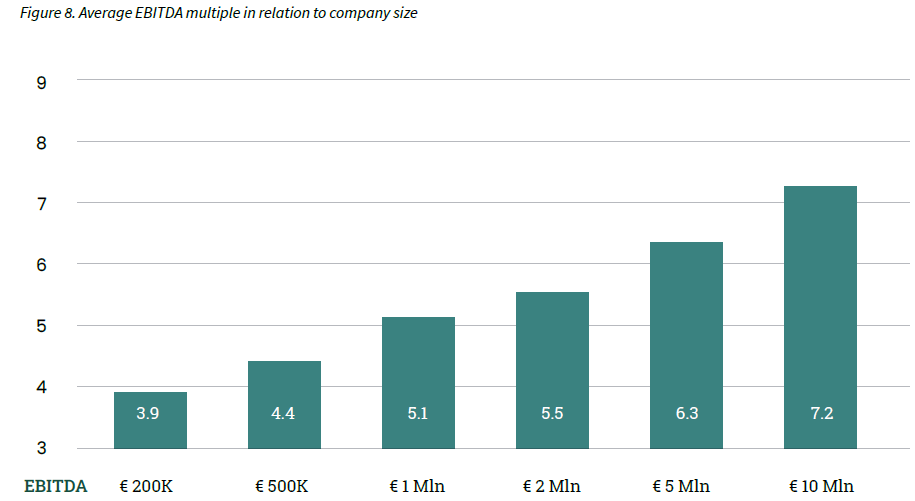

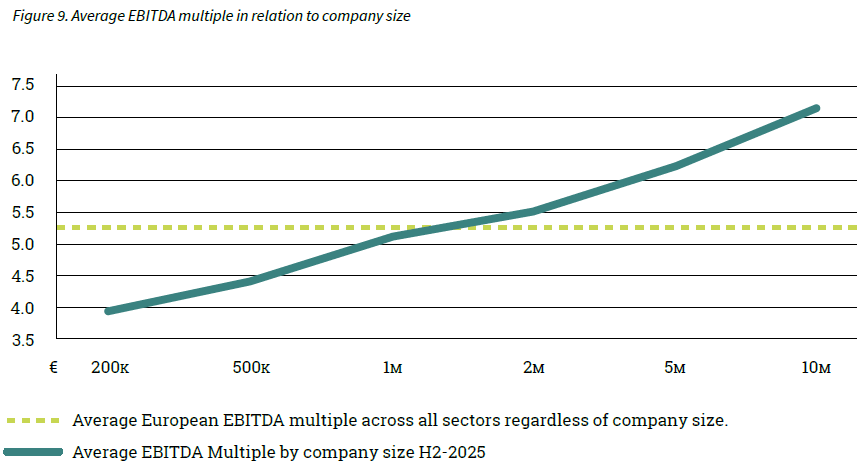

Significant difference in multiples for large and small companies

The size of a company plays a crucial role in determining multiples in business valuation. For small and medium-sized enterprises (SMEs) in Europe, it is essential to accurately quantify the impact of the Small Firm Premium. This is particularly relevant for businesses with an EBITDA ranging from €200,000 to €10,000,000.

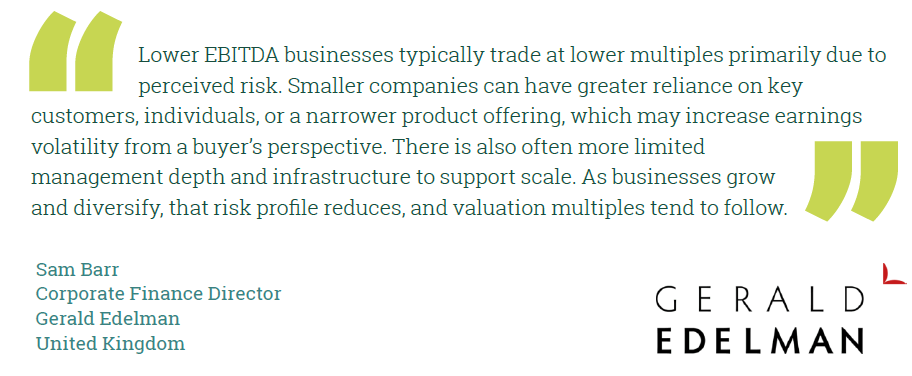

Studies have shown that smaller companies face a higher likelihood of not achieving their expected cash flows (Damodaran, 2011; Grabowski and Pratt, 2013). This can be attributed to factors such as reliance on specific customers or suppliers, or dependence on unique technical expertise that may be lost if key employees leave. Such vulnerabilities can significantly impact a company’s returns and, consequently, its valuation. The elevated risk premium associated with smaller businesses, known as the Small Firm Premium, leads to a reduction in value. As a result, EBITDA multiples for larger companies tend to be higher on average compared to those for smaller companies.

The results of this monitor survey confirm again that companies with a low EBITDA have a lower multiple than companies with a high EBITDA. The influence of company size on EBITDA multiples paid is presented in Figure 8 and Figure 9.

The difference in the EBITDA multiple between companies with a normalised EBITDA of €200,000 and €10,000,000 is 3.3 (3.9 compared to 7.2).

For companies with an EBITDA below €200,000, we do not determine a multiple for the following reasons:

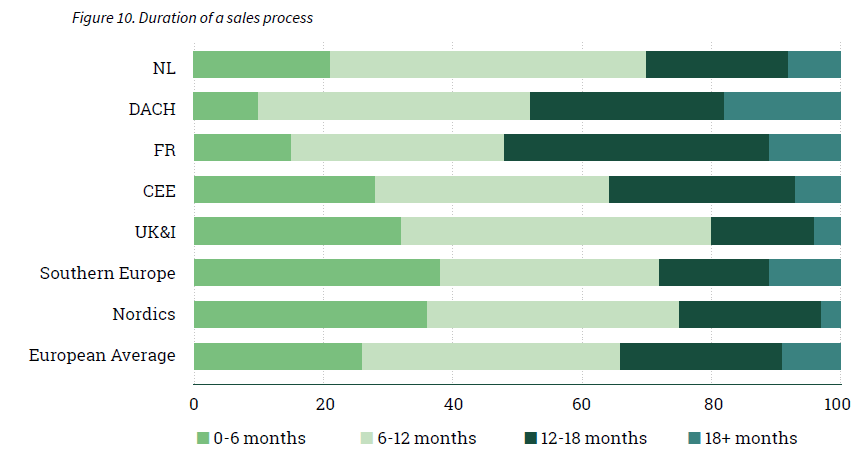

The typical SME transaction process takes around one year from mandate to closing

The duration of a sale process is influenced by factors such as market complexity, the seller’s level of preparation, and financing pressure on buyers. The lead time of a transaction, from obtaining mandate to deal closing, can vary significantly.

The lead times of sale processes are distributed on a percentage basis across the categories shown in Figure 10. The majority (66%) of sales processes guided by an M&A advisor had a duration of less than 12 months. 34% of sales processes have a duration of over a year.

Regional differences are visible. Advisors in Southern Europe, the Nordics and the UK&I report the shortest sales processes, with the largest share of transactions closing within six months. In contrast, France and the DACH region report comparatively longer deal timelines, with a higher proportion of transactions taking between 12 and 18 months or longer. The DACH region in particular stands out for the highest share of processes exceeding 18 months. Across all regions, however, the 6–12 month timeframe remains the most common duration for sales processes, indicating that the typical SME transaction process still takes around one year from mandate to closing.

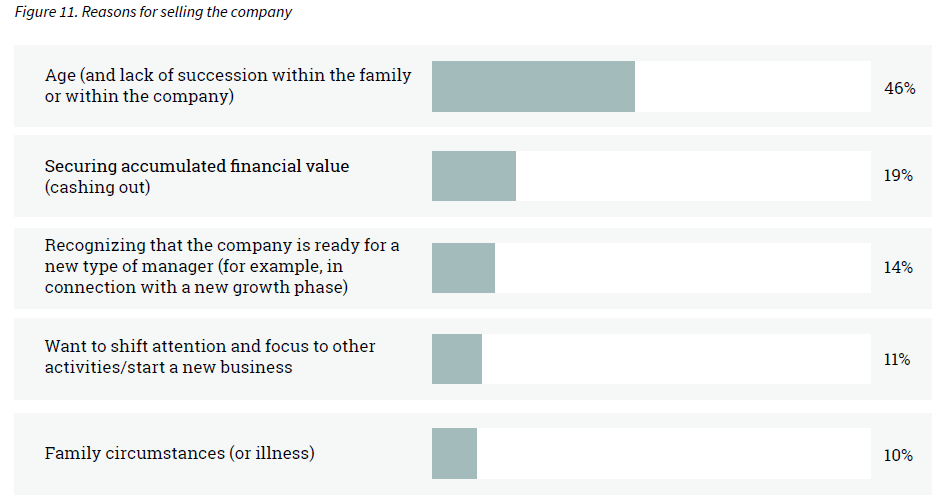

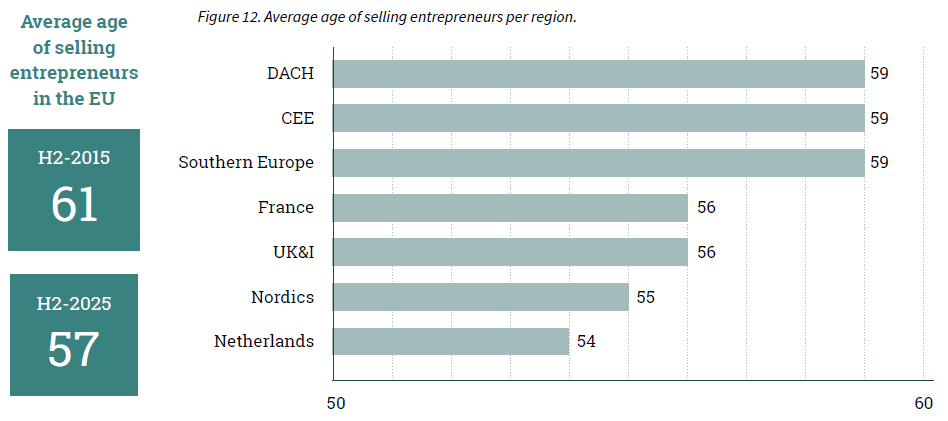

Age is the most common reason for selling a business

A company sale can be initiated for a wide range of reasons. In some cases, age plays a role and there is no suitable succession, while in others the objective is to secure the financial value built up over time. In different situations, there may be a need for a new type of management to guide the company into its next phase of growth. In short, the underlying rationale varies by entrepreneur and circumstance.

M&A advisory firms were asked to identify the primary reasons for a company sale. The following reasons collectively total 100% and are presented in Figure 11.

The average age of a selling entrepreneur has decreased

Age (and lack of succession within the family or within the company) remains the main reason for selling a business, at 46%. The European advisors were also asked about the average age of a selling entrepreneur, and what the average age was 10 years ago. Over the past ten years (2015-2025), the average age has decreased from 61 to 57.

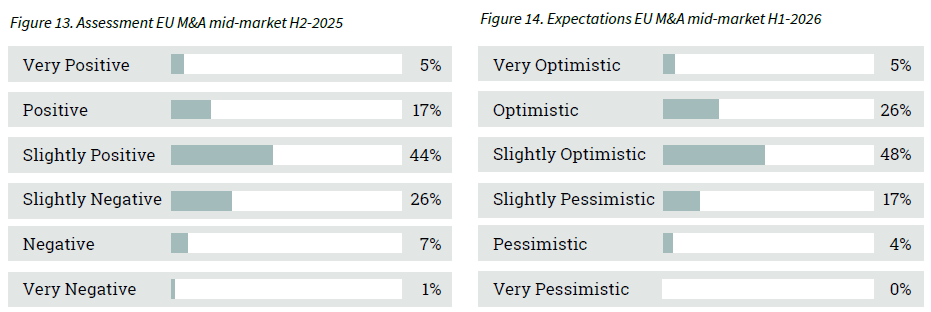

Positive assessment of H2-2025 and optimism for H1-2026

Assessing the performance and outlook of the European M&A mid-market is influenced by a range of factors, including seller willingness, access to financing, valuation expectations, and broader macroeconomic conditions. To capture both current sentiment and forward-looking expectations, M&A advisors were asked to assess the market in H2-2025 (retrospective) and provide their expectations for H1-2026 (projection).

Looking back at H2-2025, 66% of advisors viewed the market positively, while the remaining 34% expressed some level of negative sentiment, most of which was slightly negative.

Looking at H1-2026, 69% of advisors express optimism, indicating growing confidence in market conditions. Only 21% hold a more cautious outlook.

The majority of M&A transactions take place in the mid-market. This M&A Monitor uses the definition of a mid-market company as having a revenue between 1 and 200 million euros.

For this edition of the M&A Monitor, Dealsuite conducted a survey among M&A advisory firms active in the European mid-market. The survey was sent to 2797 advisory firms, which collectively represent a significant share of the regional mid-market M&A landscape. In total, 848 firms provided detailed input, resulting in a 30% response rate.

The conclusions are further supported by Dealsuite’s proprietary data and ongoing market intelligence. Together, these inputs provide a comprehensive view of current market trends, activity levels, valuation developments, and sentiment across the European mid-market M&A landscape.

This study is further supported by other regional Dealsuite M&A Monitors, analyzing the mid-market landscape in the CEE, DACH, UK&I, France, Southern Europe, the Nordics and the Netherlands.

This research was conducted by Jelle Stuij, and Roos Bijvoet. For further questions about the research, please contact Jelle Stuij. Want to know more about Dealsuite? Please contact Maarten Reinders.

.png)

Erhalten Sie relevante Einblicke direkt in Ihren Posteingang.

Alt-Heerdt 10440549 DüsseldorfDeutschland

© 2026 Dealsuite. All rights reserved.