|

Jelle Stuij

For the first time, Dealsuite has conducted a European-wide analysis of the deal terms used in share purchase agreements (SPAs) for small and mid-sized M&A transactions. This Deal Terms Report is based on firsthand data gathered from M&A legal firms across Europe, providing a comprehensive overview of market practices within the European mid-market.

The report offers insight into how often and in what way key elements, such as purchase price structures, conditions precedent, warranties, indemnities, securities, and non-compete clauses, are included in transaction agreements.

Deal terms represent the legal outcome of what has been agreed during negotiations between buyer and seller. They reflect the balance of power at the negotiating table and offer insight into the risk allocation and commercial priorities of both parties involved. As such, the structure and content of these terms can vary significantly depending on market conditions, transaction size, sector, and the specific dynamics of each deal.

This report examines the final versions of Share Purchase Agreements (SPAs) used in small and mid-sized M&A transactions across Europe, specifically those closed between July 2024 and June 2025. All transactions included in the analysis were supported by professional legal advisors, ensuring that the deal terms reviewed are representative of real-world market practice.

The objective of this research is to provide a clear overview of the current usage and negotiation of key legal provisions, such as purchase price mechanisms, conditions precedent, warranties, indemnities, securities, and non-compete clauses. The findings aim to support M&A professionals, and business owners by offering data-driven insights into how deals are structured across the European mid-market.

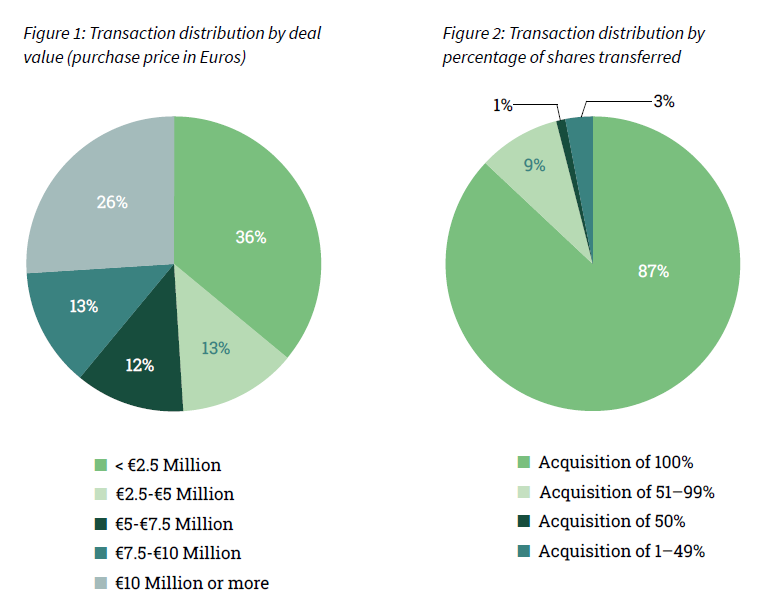

Figure 1 illustrates the distribution of reported transactions based on deal value (purchase price in euros). The survey was carried out among M&A legal offices that predominantly operate within the European mid-market.

Figure 2 presents the distribution of transactions by the percentage of shares acquired. In line with common market practice, the majority of transactions typically involve the acquisition of 100% of the shares.

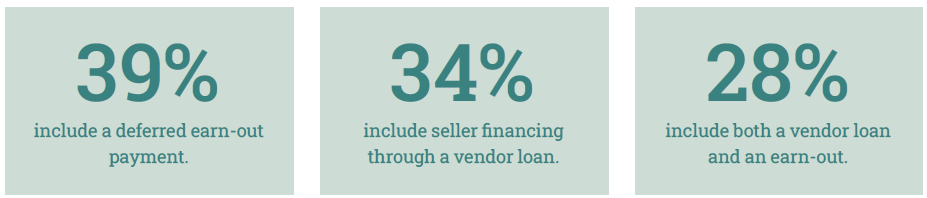

Various financing mechanisms are used to structure purchase prices in mid-market M&A transactions.

These often serve to balance risk and reward between buyer and seller, particularly in uncertain conditions. Common structures include deferred payments linked to future performance (earn-outs) and seller financing through vendor loans.

According to Dealsuite’s 2025 data (figure 3), 42% of M&A advisors reported an increase in the use of earn-outs in recent transactions. Similarly, vendor loans have become a more common financing tool, rising in popularity as higher interest rates make external debt financing more costly.

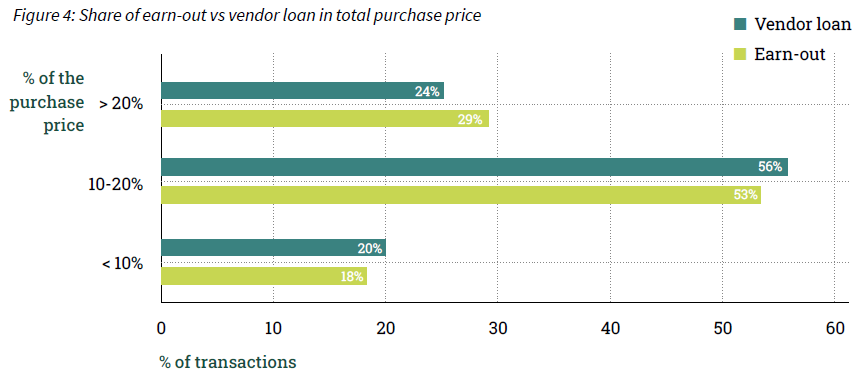

Figures 4 illustrates the typical share of earn-outs and vendor loans in the total purchase price, providing an overview of how these mechanisms are applied across transactions.

Purchase price structures define how value is transferred between buyer and seller and often reflect the balance of risk and confidence in a transaction. In mid-market European M&A, earn-outs remain a common mechanism to align post-closing interests and bridge valuation gaps.

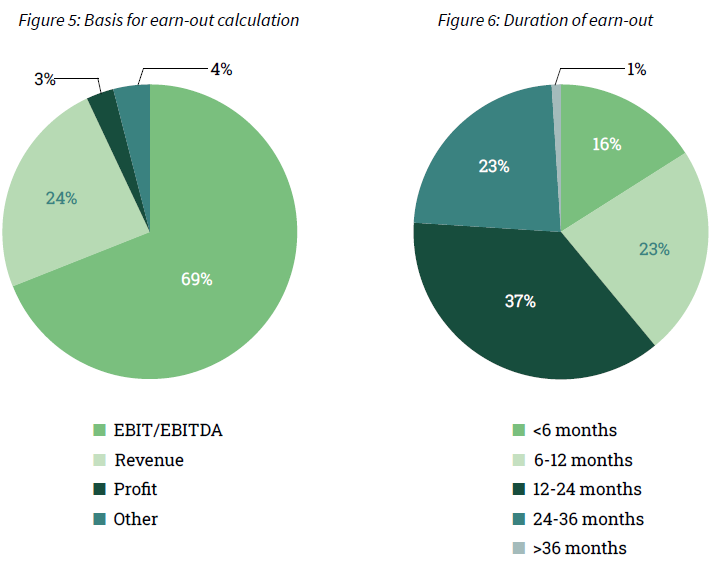

In seven out of ten transactions that include an earn-out, the deferred payment lasts between 6 and 24 months. In most cases, the earn-out is based on EBIT or EBITDA, which serves as the main performance indicator for determining the payout. Revenue-based earn-outs are less common, while only a small share is linked to profit or other performance metrics.

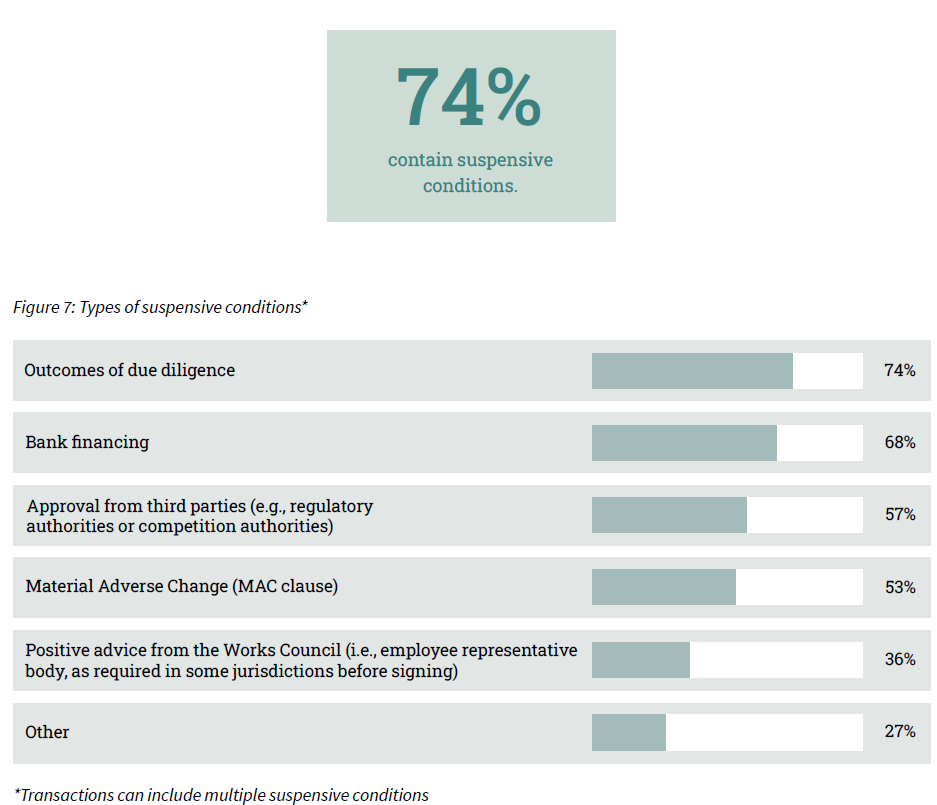

Conditions precedent outline the requirements that must be fulfilled before a transaction can be completed, serving as important safeguards for both parties. 74% of transactions included one or more suspensive conditions in the purchase agreement. Among those transactions, buyers most often waited for the completion of due diligence and the arrangement of bank financing before finalizing the deal (see Figure 7). In many cases, approval from third parties, such as regulatory or competition authorities, and the inclusion of a Material Adverse Change (MAC) clause were also key factors determining whether the deal could proceed. It is common for transactions to include multiple suspensive conditions.

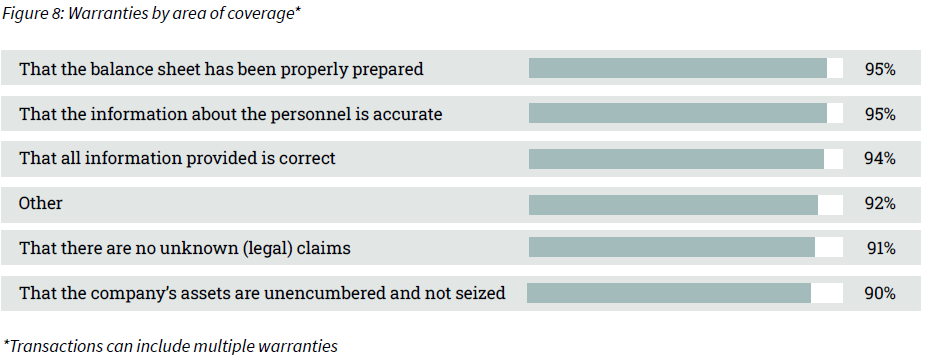

Warranties are a key element of most M&A transactions. They are used to provide the buyer with assurances about the accuracy and completeness of the information provided by the seller, and to allocate risk between both parties after the transaction. Warranties typically cover areas such as financial statements, legal claims, ownership of assets, and personnel matters, ensuring that the buyer can rely on the integrity of the company’s financial and operational position at the time of sale. According to the results of the European M&A Monitor (Dealsuite, September 2025), 30% of M&A advisors observed an increase in the application of warranties and indemnities as deal terms during the first half of 2025.

Figure 8 shows that the most common warranties relate to the proper preparation of the balance sheet (95%) and the accuracy of personnel information (95%). Other frequently included warranties cover the correctness of all information provided (94%), the absence of unknown legal claims (91%), and the assurance that the company’s assets are free of encumbrances or seizures (90%).

Indemnities are commonly included in M&A transactions to protect the buyer from potential liabilities arising from the company’s past activities. They provide a mechanism to allocate specific risks to the seller, ensuring that any pre-existing issues do not transfer to the buyer after completion. In most transactions, at least one indemnity is included in the share purchase agreement, typically covering areas such as tax, legal, or compliance-related matters. As shown in Figure 9, tax matters are by far the most common area covered by indemnities, followed by risks identified during due diligence, pensions, data privacy, and environmental issues.

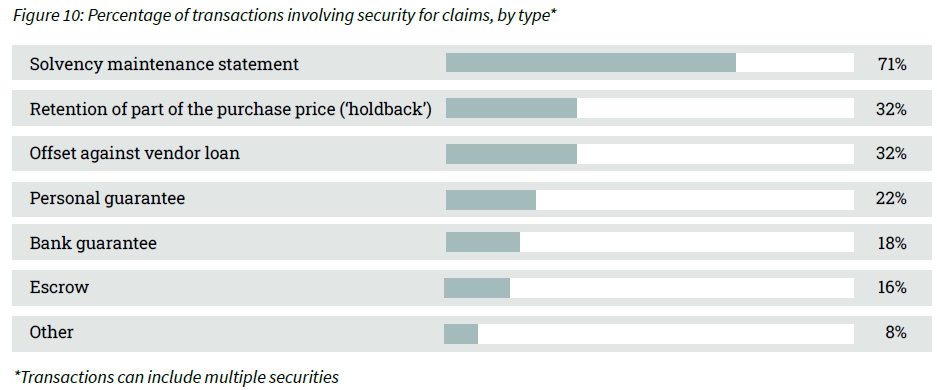

To ensure that sufficient financial resources are available from the seller in the event of a claim, securities are included in all transactions involving warranties and indemnities. Figure 10 shows that a solvency maintenance statement remains the most common form of security, applied in 71% of transactions.

Other frequently used forms include a holdback or offset against a vendor loan (both 32%), as well as personal guarantees (22%) and bank guarantees (18%).

To avoid deal term discussions, M&A insurance for SME provides a new alternative.

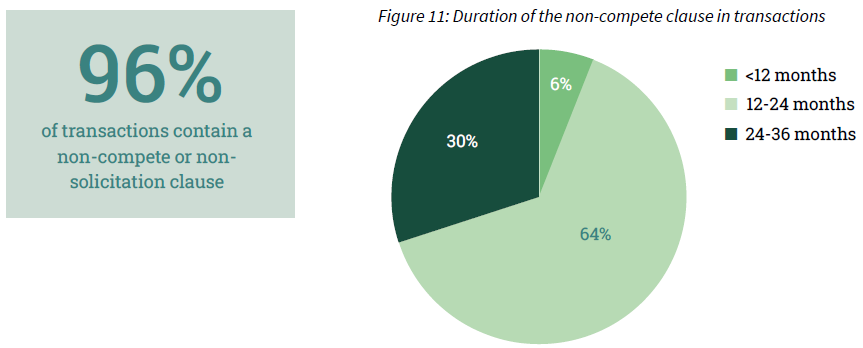

A non-compete clause is a contractual provision that restricts the seller from engaging in business activities that would compete with the company being sold for a specified period and within a defined geographical area. Its purpose is to protect the buyer’s investment by preserving the goodwill, client relationships, and market position of the acquired company.

In the European mid-market, non-compete clauses are an almost universal feature of share purchase agreements, included in 96% of transactions. In most cases, the restriction applies for 12 to 24 months (64%), though in 30% of deals the limitation extends up to three years. Such clauses often go hand in hand with non-solicitation provisions, preventing the seller from approaching former customers or employees.

The majority of M&A transactions take place in the mid-market segment. This Deal Terms Report focuses on the legal and structural aspects of such transactions, providing insight into how deal conditions are shaped across Europe.

For this research, Dealsuite conducted a survey among M&A legal firms specialized in mid-market transactions in Europe. A total of 959 firms provided detailed input based on the share purchase agreements they advised on between July 2024 and June 2025.

The conclusions are further supported by Dealsuite’s proprietary data and ongoing market intelligence.

Together, these inputs offer a unique perspective on current deal structures, reflecting real-world market practices across multiple European jurisdictions.

Focus: Mid-market M&A transactions across Europe

Regions covered: Europe-wide, across all major markets

Respondents: M&A legal firms advising on share purchase agreements

Approach: Quantitative survey on deal structures and legal terms

Data sources: Survey input combined with proprietary Dealsuite data and insights

Scope: Purchase price structure, conditions precedent, warranties, indemnities, securities, and noncompete clauses

This study is further supported by separate regional Dealsuite reports, analyzing the mid-market M&A landscape in the CEE, DACH, UK&I, France, Southern Europe, the Nordics and the Netherlands.

Additional sources used:

• Dealsuite transaction data 2015-2025

• Dealsuite M&A mid-market trends report 2025

• Dealsuite M&A Monitors 2015 - 2025

This research was conducted by Jelle Stuij and Roos Bijvoet. For further questions, please contact Jelle Stuij.

Discover how Dealsuite can benefit your business - contact Maarten Reinders, CCO

.png)

Grow your network. Find more deals.

Science Park 106

1098 XG Amsterdam

Netherlands

© 2026 Dealsuite. All rights reserved.

.png)

.png)