|

Tim Lammar

Thank you for your interest in the second M&A Monitor for Central and Eastern Europe by Dealsuite. This report consolidates research performed by Dealsuite, the leading tool for M&A transactions. It contains statistics and trends for the CEE M&A mid-market (enterprises with a revenue between € 1 million and € 50 million) over the first half of 2025.

The aim of this study is to create periodic insights that improve the CEE market’s transparency and to serve as a benchmark for M&A professionals. We are convinced that sharing information within our network leads to an improved quality and volume of deals.

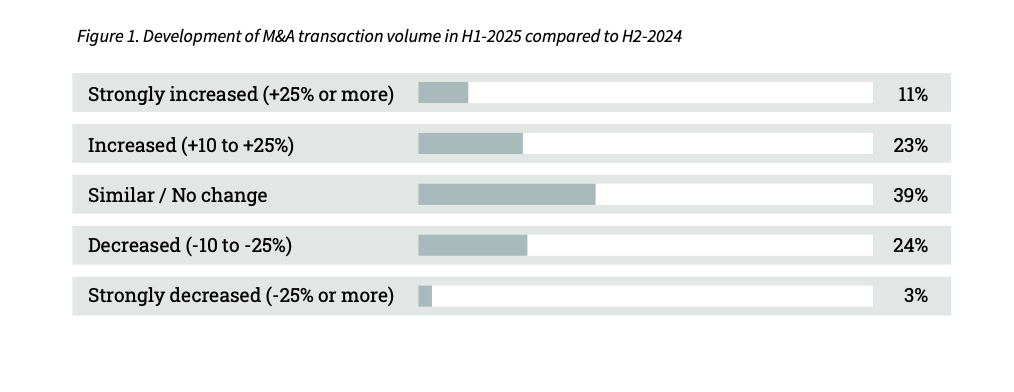

After years of turbulence, uncertainty has become less of an exception, and more of a constant. Since 2020, the M&A market has been confronted with a series of external influences: high inflation, rapidly rising interest rates, geopolitical tensions both inside and outside of Europe, and global trade wars putting pressure on economic dynamics. Where these factors previously led to hesitation among buyers and sellers, there now appears to be a structural adjustment. Many dealmakers have adapted to this new reality, where volatility is more often the rule than the exception. This adaptation marks the emergence of a ‘new normal’ that is visible across the M&A market, particularly in the SME segment, which has traditionally also been less susceptible to macroeconomic fluctuations.

Even now, the SME segment is showing a relatively stable picture, despite ongoing external uncertainties. This translates into a market that appears more resilient than before.

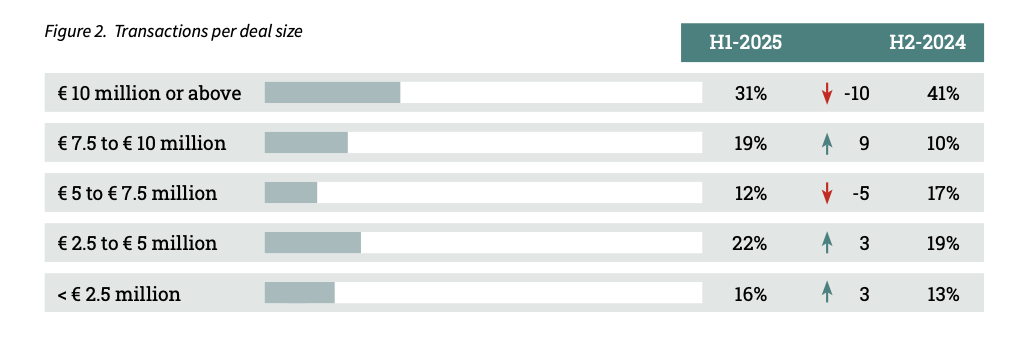

In the first half of 2025, the average deal size decreased compared to the second half of 2024, marking a shift toward smaller transactions. While deals above €10 million accounted for 41% of transactions in H2-2024, their share dropped by 10 percentage points to 31% in H1-2025. At the same time, smaller transactions gained ground, with deals between €2.5 and €5 million increasing by 3 percentage points and those below €2.5 million also rising by 3 percentage points. The only larger bracket that saw growth was the €7.5 to €10 million range, which increased by 9 percentage points.

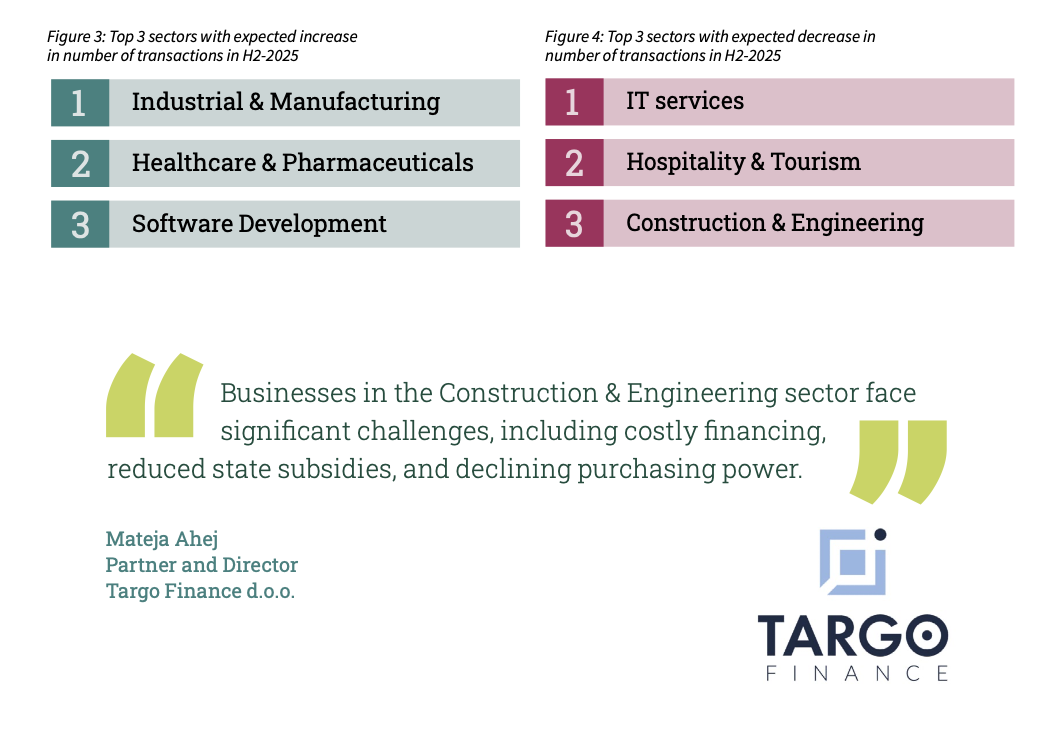

The number of expected transactions in a sector is influenced by a variety of market, industry, and financing-related factors. To gain insight into anticipated shifts, advisors were asked in which sector they expect the largest increase or decrease in the number of transactions in H2-2025. Each respondent could indicate one sector. The results are presented in two charts, showing the three sectors most frequently mentioned for an expected increase and decrease.

Industrial & Manufacturing was most frequently cited as the sector expected to see the largest increase (23% of respondents), followed by Healthcare & Pharmaceuticals (19%) and Software Development (14%). IT-services was most frequently cited as the sector expected to see the largest decrease (19% of respondents), followed by Hospitality & Tourism (16%) and Construction & Engineering (15%).

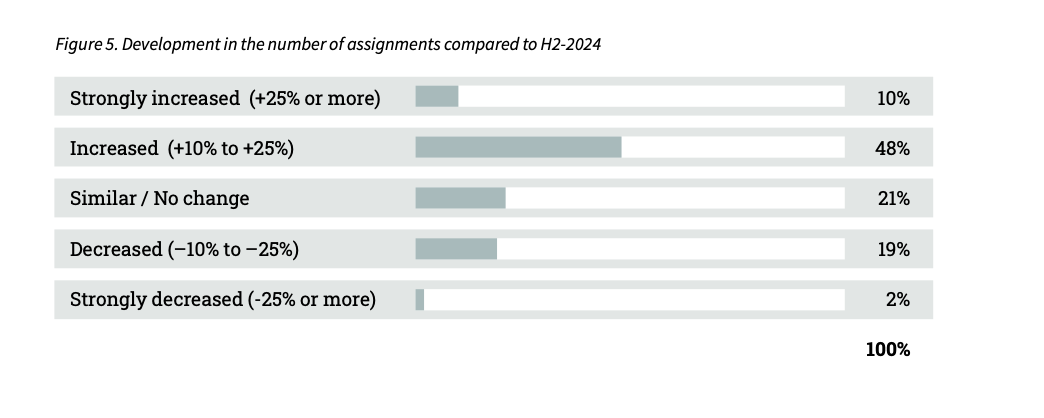

The results are explained in more detail in Figure 5 below. These are assignments received in H1-2025 and completed in H1-2025, however, it is worth noting that some of these projects may be completed during a later period or canceled. In H1-2025, 21% of advisors reported a similar number of transactions compared to H2-2024. While 21% of advisors noticed a drop, 58% reported an increase in the number of assignments.

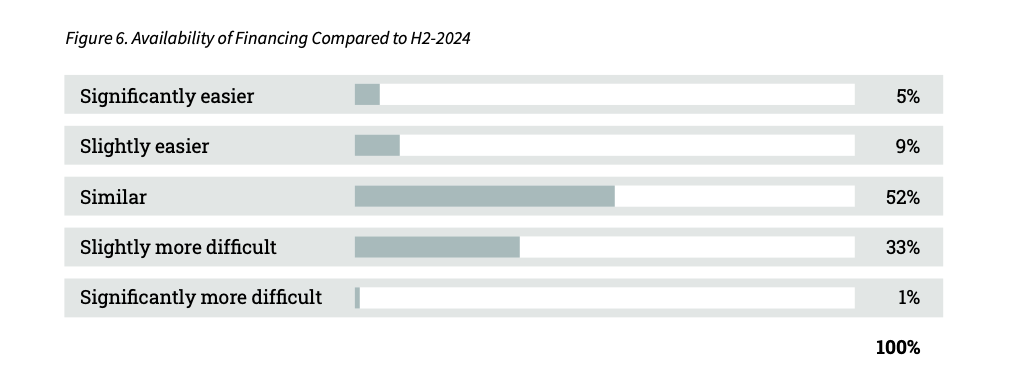

Advisors were asked to report on the availability of financing compared to H2-2024, the results are shown in Figures 6 and 7. According to 52% of the advisors, access to financing in CEE has remained similar compared to the second half of 2024. A total of 14% of respondents report that financing has become easier, whereas 34% indicate it has become more difficult.

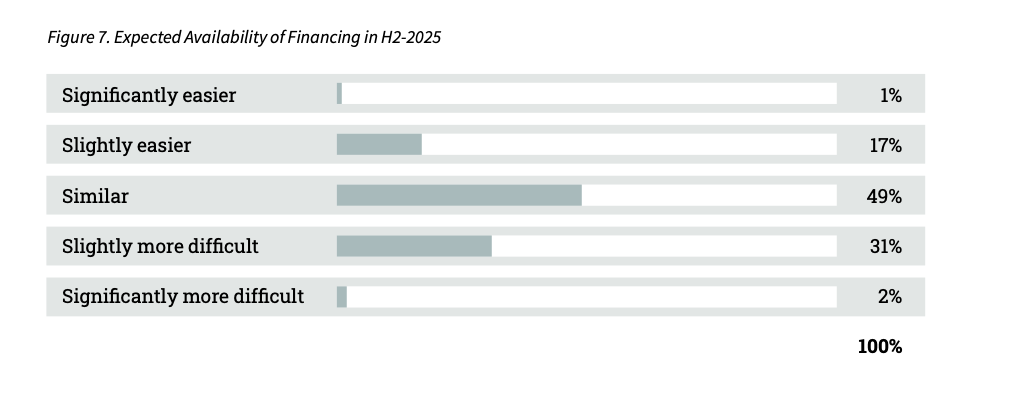

Looking ahead to the second half of 2025, respondents are split in their expectations for financing conditions. While just under half anticipate conditions to remain stable (49%), a notable share foresee some degree of improvement (18%), and a slightly larger group expect financing to become more challenging (33%).

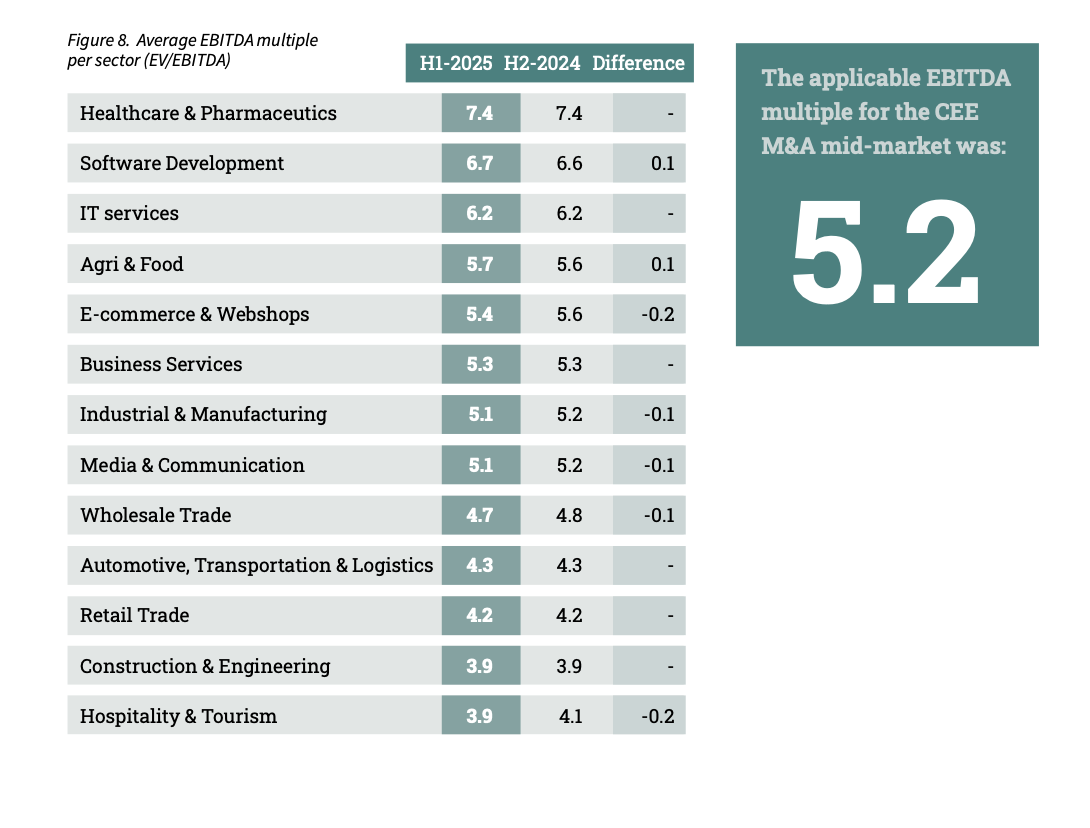

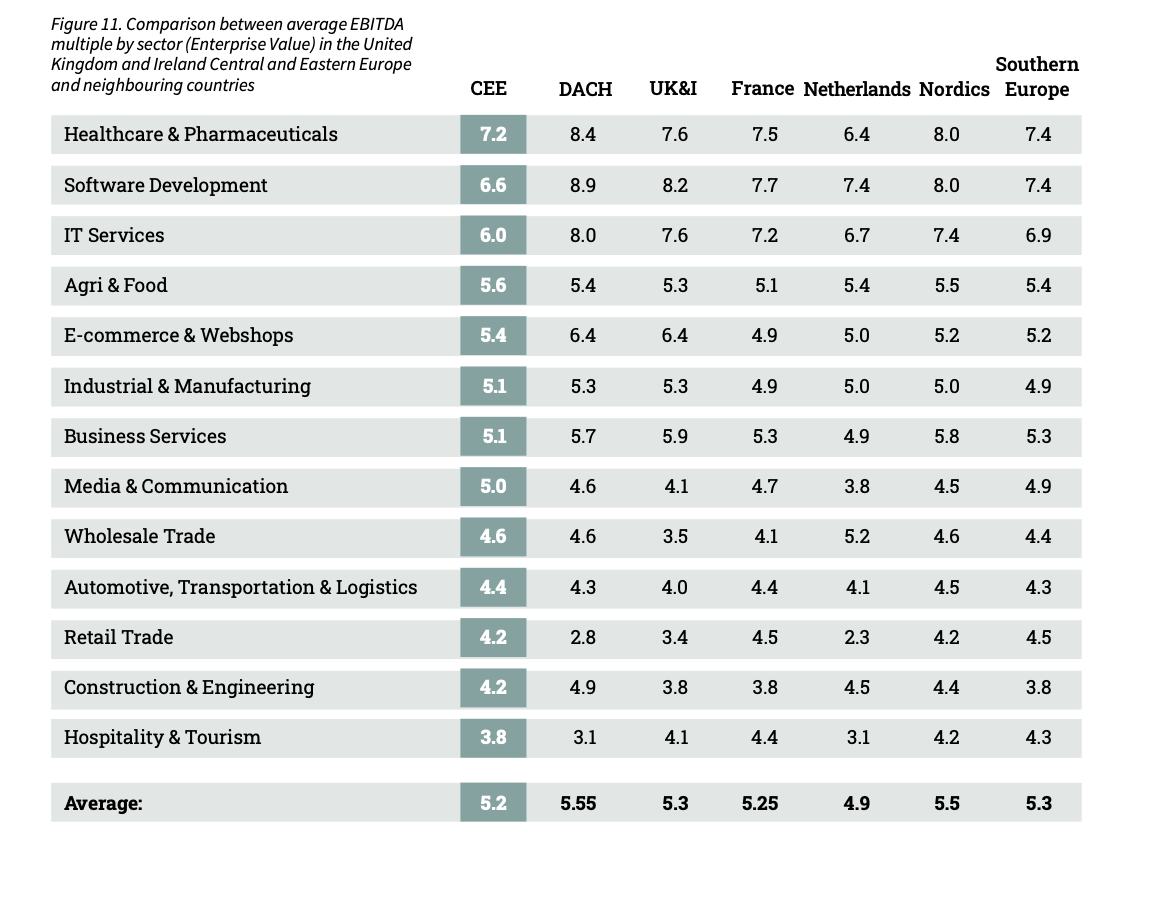

Dealsuite is reporting the average multiples per sector every six months, the average EBITDA multiple paid for a company in a specific sector. In this study, participants were asked about the current multiples being paid, based on their (revised) insights. The results are shown in Figure 8. The reported multiples are based on the enterprise value (EV) of the acquired companies.

The average EBITDA multiple slightly decreased from 5.3 to 5.2 in H1-2025. Most sector multiples saw a slight decline or remained stable. The Software Development sector and Agri & Food sector both saw an increase of 0.1.

Company valuations are inherently specific and depend on factors such as growth, profitability, market position, and risk. While a multiple alone is not a complete valuation method, it provides a useful benchmark, particularly for comparing similar transactions in the near term.

Figure 9 illustrates the distribution of EBITDA multiples by sector. Some sectors encompass a wide range of companies, which explains the broader spreads compared with sectors composed of more similar businesses. The table shows the typical range of EBITDA multiples per sector, though individual transactions can occur at significantly higher or lower levels. To provide a representative view of a typical company within each sector, the range has been adjusted to exclude the two largest outliers per sector.

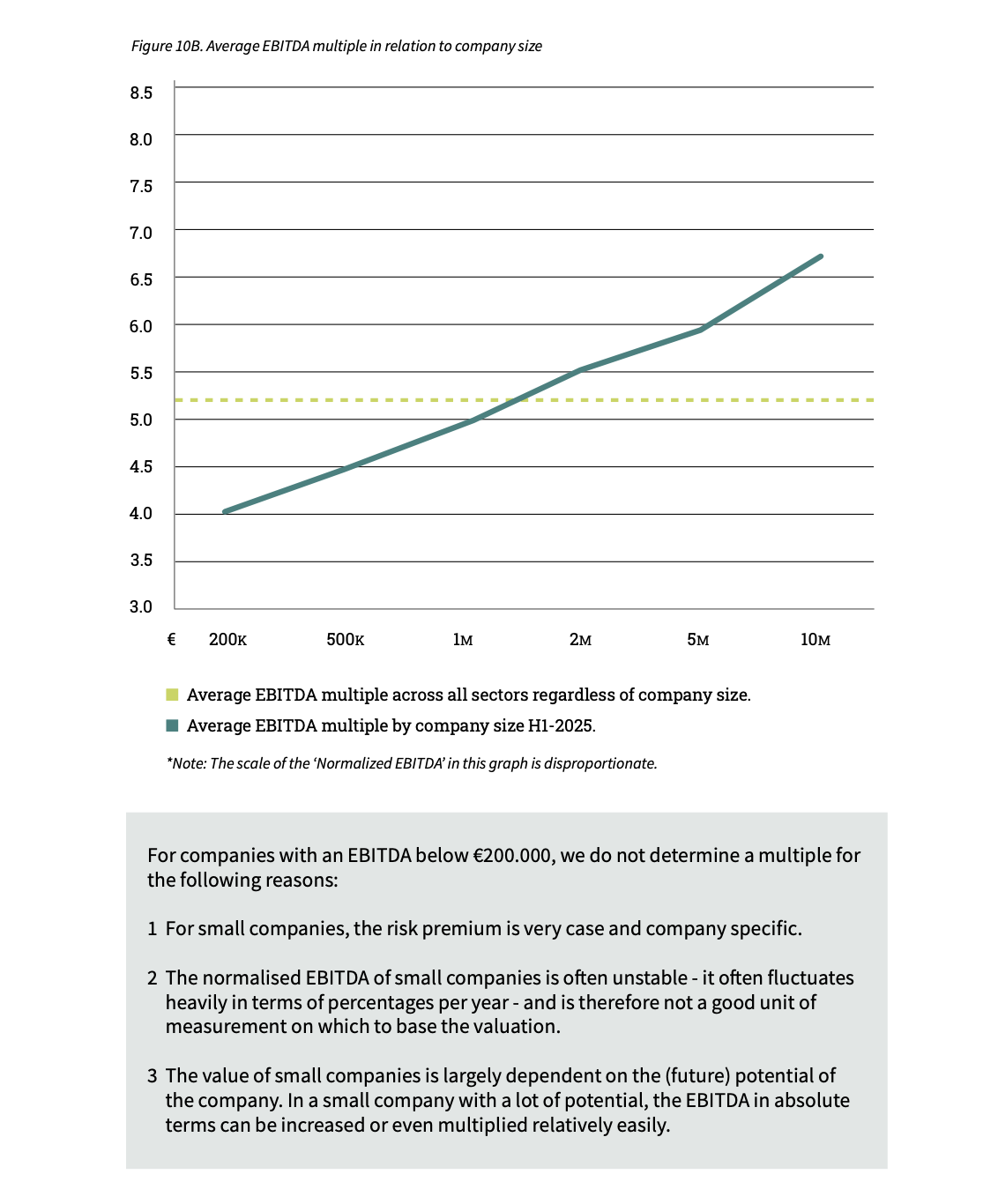

The size of a company can influence the average paid EBITDA multiple. For the first time, the impact of the so-called Small Firm Premium on the average EBITDA multiples for SMEs in Central Eastern Europe (CEE) is being analyzed. Specifically, companies with an EBITDA ranging from €200.000 to €10.000.000 are considered. This EBITDA range is a realistic representation of SMEs in CEE and is therefore used to express the size of a company.

Research has shown that the smaller a company is, the greater the chance that the expected cash flows will not be realised (Damodaran, 2011; Grabowski and Pratt, 2013). Consider, for example, the dependency on certain customers or suppliers, or the dependency on specific technical know-how that can quickly diminish when staff leave. This can have a significant impact on the returns and thus on the value of a company. The higher risk premium that applies to smaller companies (the so-called Small Firm Premium) causes a value-reducing effect. As a result, the EBITDA multiples paid for larger companies are on average higher than the multiples paid for smaller companies.

The results of this monitor survey confirm that companies with a low EBITDA have a lower multiple than companies with a high EBITDA. The influence of company size on EBITDA multiples paid is presented in Figures 10A and 10B.

The difference in the EBITDA multiple between companies with a normalised EBITDA of €200.000 and €10.000.000 is 2.7 (4 compared to 6.7).

A comparison of EBITDA multiples between different countries highlights the advantages of cross-border deals. For example, it can be beneficial to buy a particular company abroad, or to sell a company to an international buyer. Figure 8 shows the differences in EBITDA multiples between European markets.

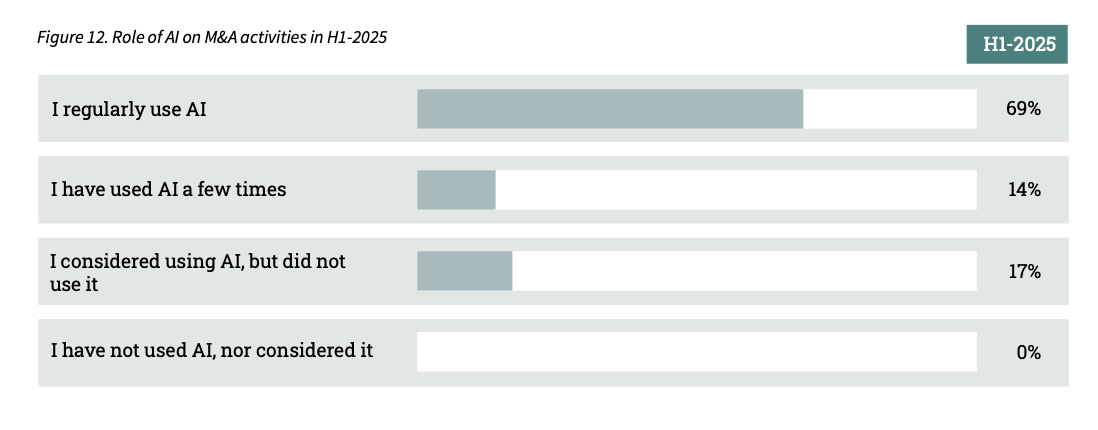

In the first half of 2025, AI has established a strong foothold in M&A activities across the CEE region. Nearly seven in ten respondents (69%) report using AI on a regular basis, while a further 14% have experimented with it a few times. Only a small minority have not yet adopted AI, indicating that its role in the M&A process is already widely recognized.

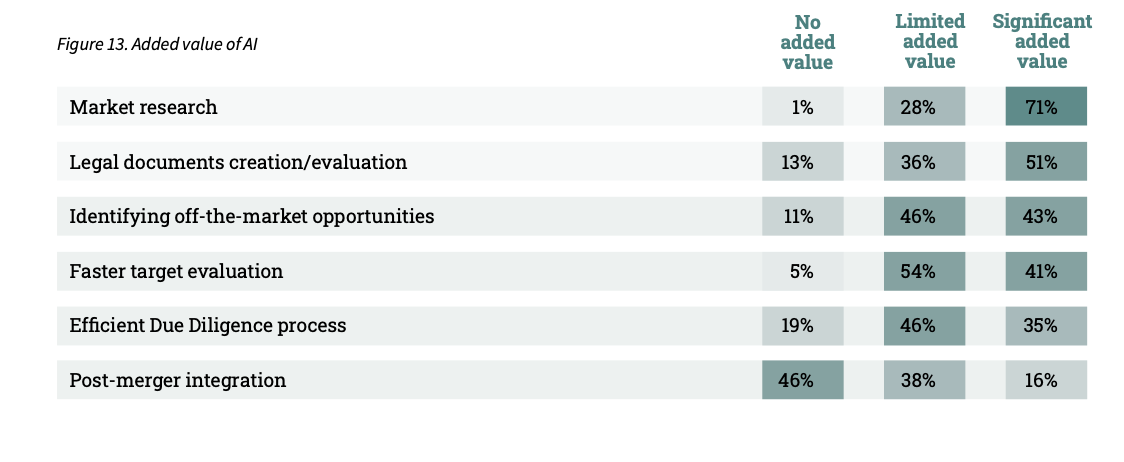

In H1-2025, AI is perceived as adding the greatest value in market research, where 71% of respondents report significant value. Strong results are also seen in identifying off-market opportunities and in faster evaluation of targets, with majorities recognizing at least some added value. In contrast, the role of AI in due diligence and legal documentation is viewed as more limited, with fewer respondents seeing significant value. Post-merger integration remains the area where AI is least impactful, as nearly half of advisors report no added value.

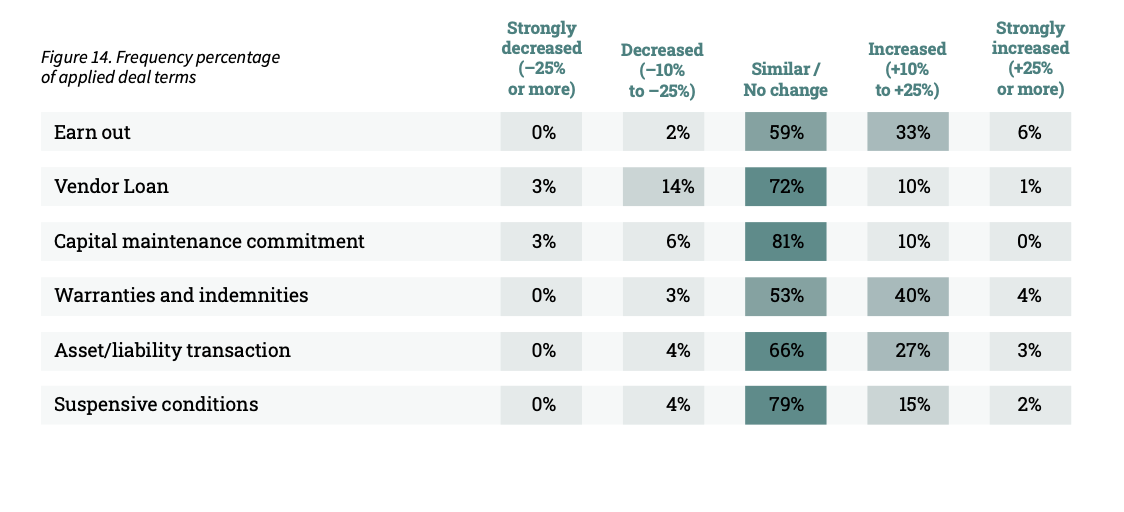

Macroeconomic developments can influence the use of specific deal terms. In this edition of the M&A Monitor, the application and frequency of various deal terms were analyzed (Figure 14). In H1-2025, the use of most common deal terms in CEE remained broadly stable compared with H2-2024. Warranties and indemnities were widely applied, with 53% of respondents reporting no change and 44% indicating an increase. Earn-outs also gained traction, as nearly 40% of respondents observed higher usage. By contrast, vendor loans and capital maintenance commitments showed little movement, with the vast majority reporting no change. Asset/liability transactions saw a modest increase, noted by 30% of respondents, while suspensive conditions were largely stable with only limited upward shifts.

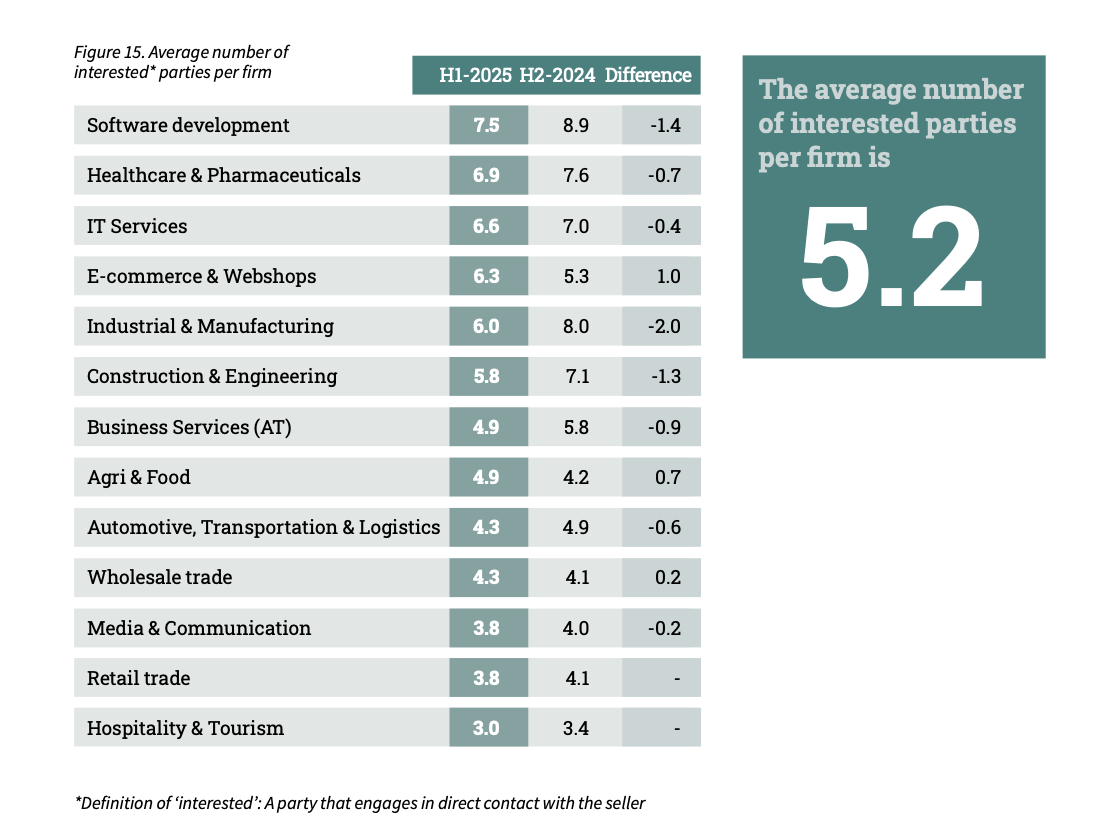

The M&A market is a ‘sellers market’. The balance between supply and demand in the M&A market varies by sector. M&A advisory firms were asked to indicate, for each sector, how many serious potential buyers typically show interest in a company that is put up for sale. The results are presented in Figure 15. Various factors can influence the number of interested buyers. This is affected, among other things, by financing conditions, economic uncertainty, or sector developments that impact buyer appetite. On average, there were 5.7 interested parties per offered firm in H1-2024. In H1-2025, that number slightly decreased to 5.2 interested parties per offered firm on average.

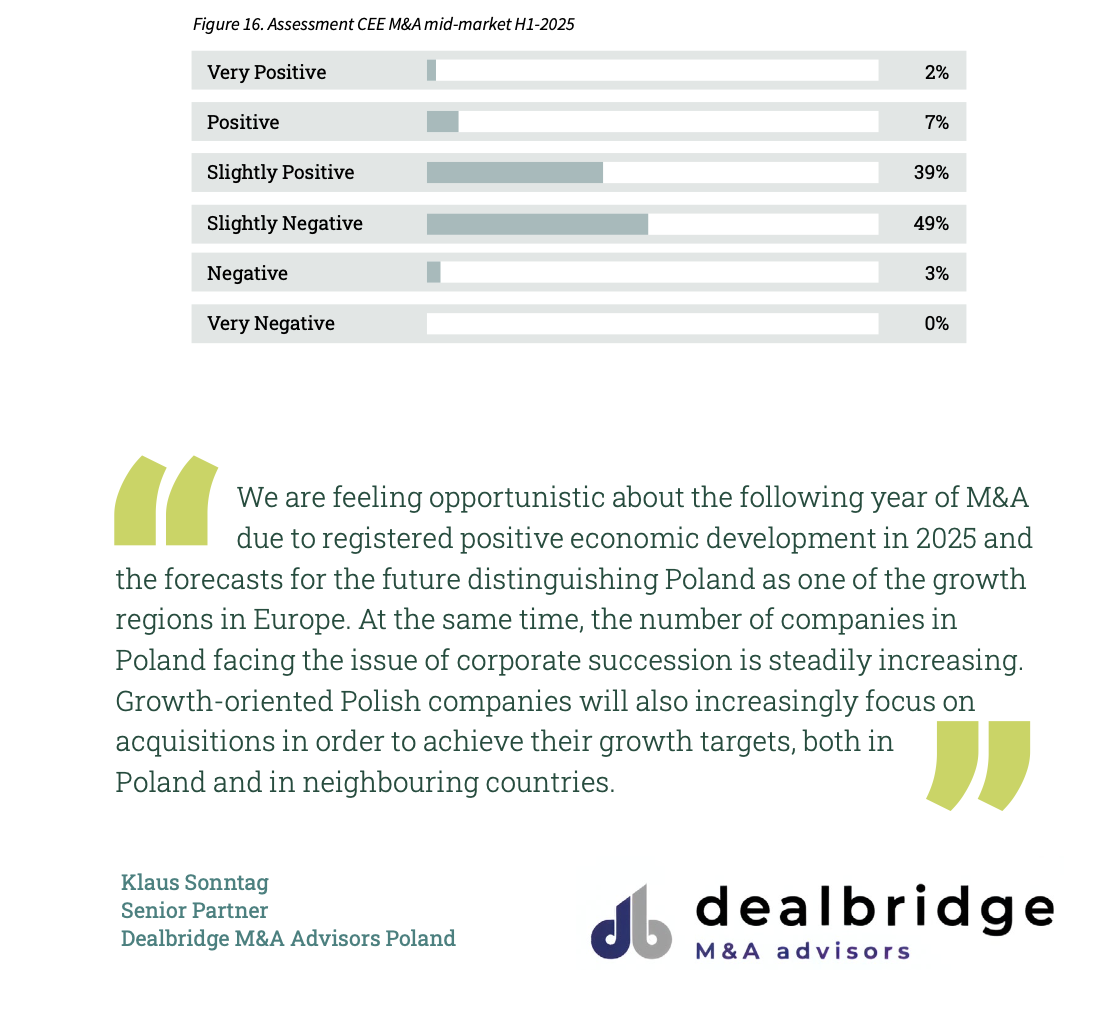

Assessing the performance of the CEE M&A mid-market is based on many factors, including the willingness of entrepreneurs to sell their businesses, funding availability, macroeconomic developments etc. An interpretation of these factors is needed to determine how the market will develop. The survey included both assessments of the M&A mid-market in H1-2025 (retrospective) and H2-2025 (projection).

The advisors were asked to evaluate the performance of H1-2025. The responses were mixed, with close to half of the advisors looking back at H1-2025 with a satisfied feeling, and 52% of respondents looking back with a rather negative feeling.

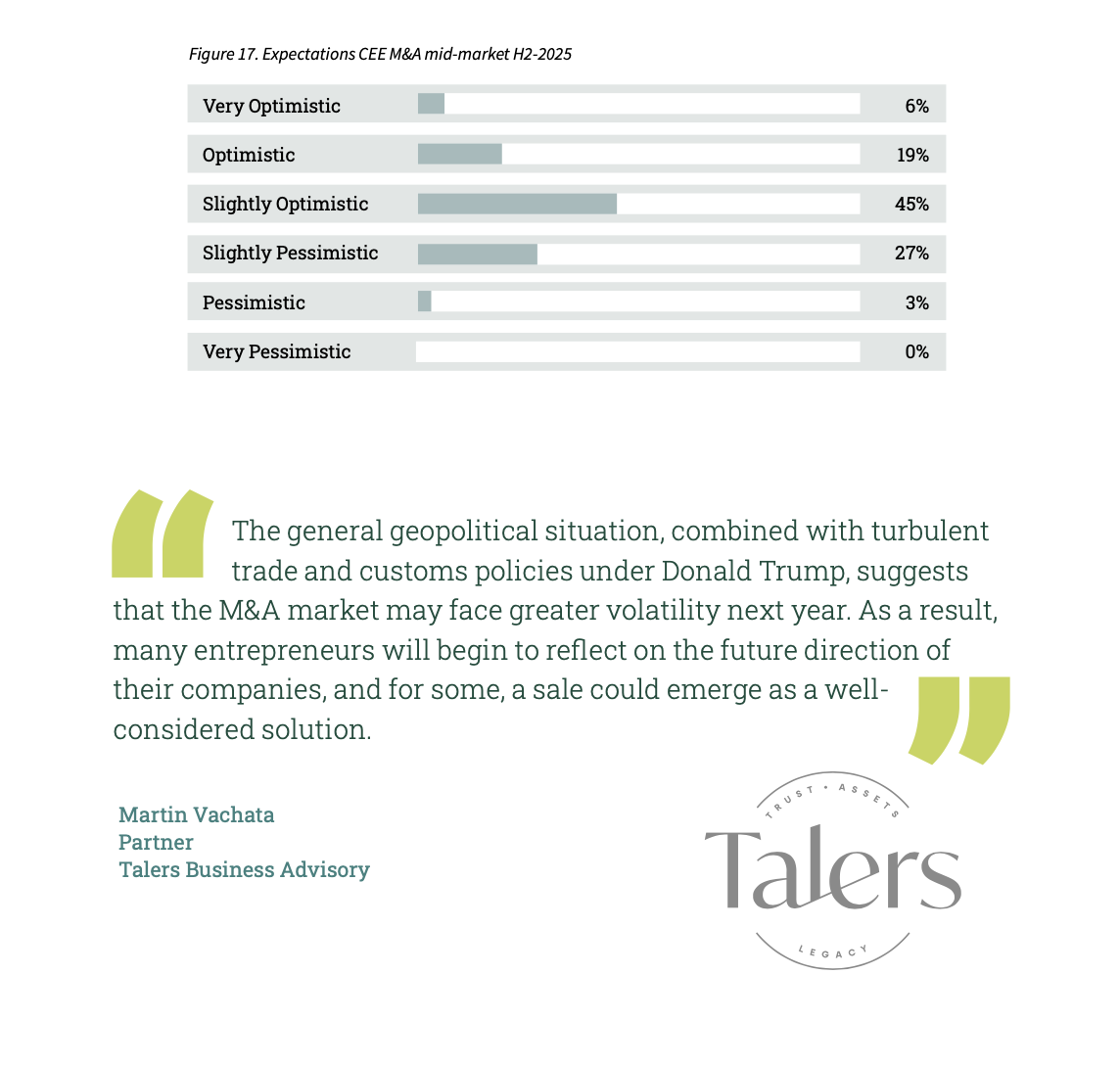

The outlook for H2-2025 is more promising, with 70% of advisors sharing an optimistic expectation for the coming half year.

The majority of M&A transactions take place in the mid-market. This report uses the definition of a mid- market company as having a revenue between €1 and €50 million. The survey was sent to 452 M&A advisory firms. Considering their combined input, they represent an essential part of the M&A mid-market in Central and Eastern Europe. Out of the total of 452 advisory firms, we received 107 respondents (24% response rate).

Sources used:

• 107 survey responses from key CEE M&A advisory firms

• Bain & Company. (2023, March 28). How companies got so good at M&A.

• Damodaran (2011). Equity Risk Premiums (ERP).

• Dealsuite M&A mid-market trends report 2025

• Dealsuite M&A Monitors 2015 - 2025

• Dealsuite transaction data 2015-2025

• Field, A. (2011) Discovering Statistics SPSS. Third edition, SAGE publications, London. 1 -822

This research was conducted by Jelle Stuij, and Roos Bijvoet. For further questions, please contact Jelle Stuij. For further information about Dealsuite, please contact Tim Lammar.

.png)

Grow your network. Find more deals.

Science Park 106

1098 XG Amsterdam

Netherlands

© 2026 Dealsuite. All rights reserved.

.png)

.png)